This is a retired estate. blog.cfi.co was published between 2019 and 2026, largely outside CFI.co’s editorial process: much of it was templated, and part of it was supplied through a third-party content agency’s account. It also carried republished CFI.co editorial material. It is not governed by the CFI.co governance file and it is not part of CFI.co’s hashed public archive. Publishing here stopped on 30 July 2026.

193 links across 139 posts on this subdomain were commercial placements and carried no disclosure at the time. In July 2026 each link was marked. This notice is the disclosure; the posts do not carry individual dated notes. Nothing has been deleted or unpublished: every page remains at its original address.

There are three major reasons for central banks to engage on climate change issues. The first is the set of – physical and transition – risks to financial stability potentially brought about by natural disasters and trends derived from climate change. Second, the potential impact of climate change shocks and trends on economic growth and inflation and, therefore, on their monetary policy decisions. Finally, the possibility of using their balance sheets and their macroprudential toolkit to favor climate mitigation.

Are you considering opening your first bank or looking for one for your child? Don’t just go with the one down the block due to convenience. There are actually more options out there than you realize – and some that can save you money and keep your cash safer for the long term!

Read on for our top tips on what to look for in a bank so that you can store your wealth the smart way.

1. What Kind of Account Do You Need?

Some banks offer you more perks for checking accounts versus savings accounts, and the other way around. This can be due to higher interest rates, convenient mobile checking deposit options, or banks that don’t charge you monthly fees.

If you don’t want your money to stagnant in a savings account and want to save more, then a high-interest savings account may be for you. Although many brick-and-mortar banks don’t offer very high interest, many online banks do.

Perhaps you want to replace your current checking out. Larger banks offer more options if you want flexibility, and there are also high-yield checking accounts that are offered by online banks, credit unions, and community banks.

2. Avoid Minimum Balances

Some banks require you to have hefty minimum deposits, which essentially locks your money up in an account for the foreseeable future without earning much interest. Online banks such as Ally Bank and Capital One 360 offer checking accounts that don’t require a minimum balance. Smaller banks and credit unions are also less likely to require minimum balances.

3. Avoid Overdraft Fees

Overdraft fees are one of the biggest penalties to hit consumers. Banks can charge $35 or more for each overdraft to your account if you’ve opted for overdraft protection, which can become a vicious cycle. The bank is essentially giving you a loan with a hefty fee attached.

Overdraft protection isn’t required, even though banks will try to push you towards it. When you don’t have overdraft protection, your purchases or ATM withdrawals are simply declined if you have insufficient funds. Remember to read the fine print of whichever bank you choose and go with the option that has fewer fees, or no fees at all.

Some banks will allow account holders to link a savings account or credit card to your account and transfer money if you have insufficient funds. You’ll avoid large fees, but you’ll also be able to complete your purchases.

You’ll also want to see if your bank is capable of sending you text alerts if you have a low-balance or have crossed a threshold you’ve indicated. With banks that offer mobile apps, you’ll have a much easier time monitoring your account’s balance.

4. Consider Accessibility

Although online banks come with a lot of perks, they can lack the convenience of big brick-and-mortar banks. If you’re having issues with an account or need to deposit cash, this is much easier with a traditional bank.

Many online banks require you to mail in your cash if you need to make a deposit. If you’ve noticed any fraudulent activity on your account or need some assistance, you’ll need to chat with a customer service representative online or call. Depending on how effective their customer service is, this can either be a convenience or a major hindrance.

Carefully think about your accessibility needs and choose the bank that makes your life easier for the longterm.

5. Consider Spending Habits

You’ll also want to consider your lifestyle. If you’re making an effort to save money, many financial advisors recommend you go with a bank that allows you to open and name multiple accounts. This enables you to have one checking account and separate savings accounts for all your different savings goals, such as emergency money, gift funds, and travel funds.

Portioning out your money this way makes it far easier to budget. When you access your account online, you’ll see right away how much money you have available to spend and how much you need to save.

6. Digital Features

There are a lot of digital features available now that make your life a lot easier and your account more secure. This includes the ability to transfer funds, deposit checks, and pay bills all through an app.

Some banks offer the ability to immediately lock a debit card or customize it to not allow international purchases or purchases out of your local area. Overall, banks are pushing towards more high-tech solutions, including utilizing IoT.

If you’re predominantly a debit card user, this kind of peace of mind is invaluable. Make sure to browse a bank’s website and read their app reviews to see how convenient and developed their digital features are.

7. Read Terms & Conditions

It may seem unnecessary, but you really should read the fine print before opening a bank account, especially one that you’ve found online. Here are a few things you should check for:

Monthly service fees

Out-of-network ATM charges

FDIC insured savings accounts

Promotional deals that are expiring

You need to know exactly what you’re getting into before you join a bank or open one for your child – this saves you future headaches. If you find that you want to open a checking account with one bank and savings with another, ask yourself if this will suit your lifestyle and if you’d be able to keep up with it.

What to Look for in a Bank: Secure Money that Grows

When you consider what to look for in a bank, it’s all about finding one that suits your lifestyle, keeps your money secure through insurance and smart digital features, and doesn’t let your money stagnate.

For instance, if you have thousands of dollars worth of savings, keeping it in a savings account with a low interest rate for years will actually be losing you money. Inflation rates rise while your purchasing power diminishes. You would do better to store this in a CD or high-interest savings account.

If you have a teenager that’s opening his or her first bank account, maybe they would do better with an account that offers the ability to open multiple savings accounts. This will help them learn how to budget effectively.

If you found this article helpful, keep reading our banking section for the latest news and analysis of banking policies around the world!

Few

theories have caused so many discussions as the Modern monetary theory (or MMT),

which has been popularized by the leftmost sector of the Democratic Party, US, when

it recurred to it to defend the huge expenses of the federal government on an

attempt to detoxify the country from the fossil fuels and to finance a Medicare

coverage for all.

The re-birth of the Modern

Monetary Theory

MMT was

created in the 1970s by the American economist Warren Mosler and shows

similarities with older schools like Chartalism and Functional Finance. It was congresswoman and activist

Alexandria Ocasio-Cortez who brought the debate to the table. In January 2019,

she claimed that the government should implement Modern Monetary Theory to

finance the Green New-Deal, applying political measures similar to those of the

1930s to augment the expenses but for ecologic reasons. In a public interview, she expressed that MMT should “be

a larger part of the conversation.”

The approach

Despite the

complexity and debate around MMT, there are some basic concepts shared by most

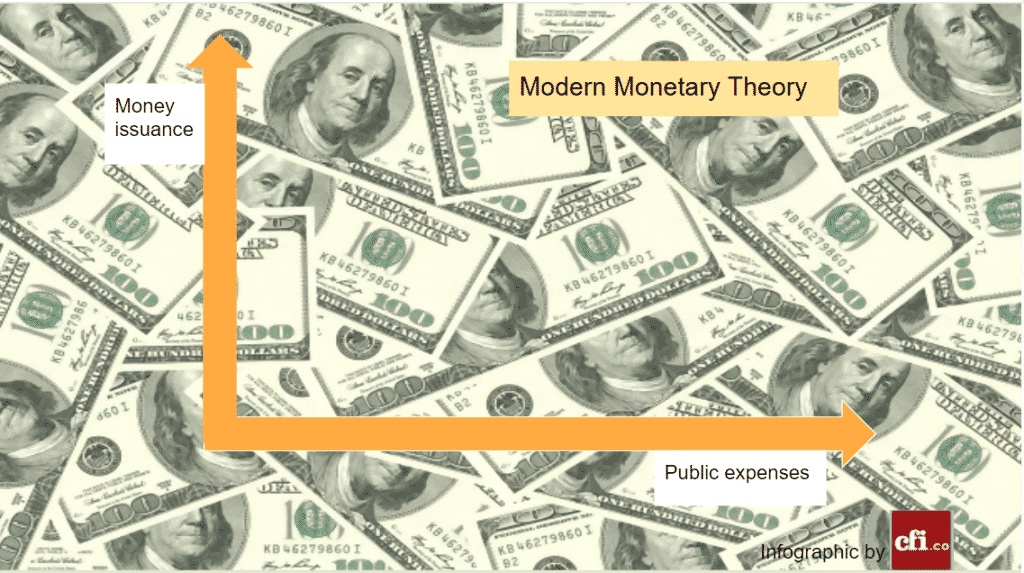

of its adepts. The fundamental idea is that since the abandonment of the gold

standard, a sovereign estate can print as much money as needed to finance

public expenses and inject money into the economy, which they later withdraw in

taxes. They sustain that governments

cannot go broke, as they can always create more money to pay off debts.

According

to MMT theorists, we have been misled to think that substantial government debt

is followed by financial collapse. Moreover, they state that if the spending

creates deficit, it isn’t a real problem, as the national deficit is, in fact,

the private sector’s surplus.

Modern Monetary Theory and

inflation

Mainstream

economists argue that it is ridiculous to think that central banks can finance

massive spending without causing high inflation or even hyperinflation. Modern

Monetary Theory, on the other side, reckons that there is a direct relationship

between the circulation quantity of money and the level of prices. Yet,

although they recognize the risk of inflation, they see it as a constraint that

will keep decision-makers honest. Inflation is perceived as a result of real

resource limits, and the Congress should set the spending, tax, and industry

policies to keep inflation under control.

Restrictions on Modern monetary theory

Modern

Monetary Theory advocates state that governments don´t have a budget constraint,

and the only limit they have is the availability of real resources, like

supplies and workers. If government spending is excessive in relation to the

available resources, inflation could occur; therefore, the importance of proper

policies.

It´s

undeniable that Modern Monetary Theory keeps gaining attention and adepts,

especially in the progressive political sectors. However, they haven´t provided

a convincing response to the inherent problem of inflation yet.

Is Modern Monetary Theory the panacea that will solve the world´s woes? Or is MMT just a new buzzword that keeps rising popularity? Implementing it would be a bold, risky experiment with no point of return or the miracle-solution we all crave for?

Will growth continue to slow, or will Europe fall into recession as global economic risks overtake it? Whatever the result, rather than being a distraction from politics, the economy will probably intensify the political challenges.

Economic Growth continues to slow

The Euro Area is heading for a second straight year of slowing economic growth. In 2017, GDP growth was at 2.4%, while 2018 is expected to be around 2%. In 2019, the IMF has forecast 1.9% (World Economic Outlook, Oct 2018), while the World Bank has forecast 1.6% in 2019, 1.5% in 2020, and 1.3% in 2021 (Global Economic Prospects, Jan 2019).

Some key countries will fare worse. Germany and Italy recorded negative growth in the third quarter of 2018, with notable decreases in industrial production. In contrast, EU members in Eastern Europe are experiencing strong growth.

Slower growth in the Euro Area is not in itself cause for concern. Despite the downward trend and negative growth in Germany and Italy, the forecasts represent continued solid economic growth. The underlying fundamentals are robust for most countries: inflation is under control, consumer spending is healthy, and Euro Area unemployment is at 10-year lows. The Euro Area looks set to add to the five straight years of growth since 2014.

Europe’s slowing growth must be seen in the context of increasing global risks to economic growth. These include the risk of a US recession,

aggressive US trade policies, and the risks from further tightening by the US Federal Reserve. If any of these risks are realised, Europe, particularly the Euro Area, may fall into recession.

The US economy appears very strong with low inflation and a strong labour market, but the stock market correction from August 2018, and the flattening (and sometimes inverting) yield curve for US treasuries suggests that the US markets are predicting slower growth. Many market-watchers are spooked by the possibility of a recession in 2019 or 2020. A US recession may become a self-fulfilling prophecy.

US trade policies entered a new era in 2018 with the March tariff on steel and aluminium, renegotiation of NAFTA (now USMCA), and the trade skirmish with China. The US has demonstrated that it will play hard on trades issues, even with traditional allies such as Canada and Europe. The steel and aluminium tariffs have had a negative impact on European exports. More tariffs cannot be ruled out.

Europe also needs to be prepared for any collateral damage from a potential trade war between the US and China. Comments after the G20 meeting in Buenos Aires gave hope of a resolution but subsequent reports suggest that negotiations will be complex, particularly as the US leverages a stronger hand with probable slower growth in China.

Another key global risk is continued monetary tightening by the US Federal Reserve in 2019, and the ensuing risk of financial contagion for, and from, emerging markets. Last year marked the long-feared end of cheap liquidity in emerging markets. As the US Federal Reserve tightened liquidity, countries like Argentina and Turkey were put into a tail-spin by markets. Advanced economies, including those in the Euro Area, remain vigilant for any potential financial contagion from emerging markets. Fed chair Jerome Powell has since tried to tone down any hawkish sentiment, and will proceed with more care. The world will be watching the Fed even more closely in 2019.

What can Europe do about recession?

If any of these global risks are realised and the Euro Area falls toward recession, what can Europe do? The ECB and national policymakers appear to have few working levers to stimulate growth. The official ECB interest rate has been below zero since 2014, while the ECB capped Quantitative Easing at the end of 2018. The ECB’s rate would thus need to rely on tools at the margins such as a new round of Targeted Longer-Term Refinancing Operations (TLTROs): discounted multi-year loans to banks. Perhaps the ECB’s biggest remaining lever to mitigate any recession is to do nothing, refraining from raising interest rates in 2019.

Unlike 2007 and 2008, many European governments (including France, Italy, and Spain) have few fiscal buffers to deal with any potential recession in 2019 or 2020. Italy has a public debt to GDP ratio of 133%, Spain 98.8%, and France 97.7% (latest figures are from 2017). Countries such as Germany and the Netherlands do have fiscal buffers, but they alone cannot mitigate a Euro Area-wide recession.

The lack of fiscal buffers will probably feed back into domestic political pressures and anti-EU rhetoric. In the event of a recession, countries with little fiscal space will be tempted to increase their fiscal spending beyond comfortable levels, which will incur the ire of the ECB, and the more fiscally conservative countries in the EU. Local leaders may then deflect this by stirring up anti-EU sentiment – a familiar path. As the economy re-emerges as a key focus, the tensions between many governments, like the new government in Italy, and the EU will probably intensify.

Need for productivity growth to get out of Europe Recession

Beyond mitigating the next recession, what Europe (and all advanced economies) really need is a new wave of structural reforms to reignite productivity-led economic growth. This includes Labour market reforms to increase flexibility and participation, as well as productivity through better vocational education and technology.

In 2017, French President Emmanuel Macron introduced labour market reforms. These included changes to the funding of vocational education and the capping of awards for workplace disputes settled in court. These have already had a positive economic impact, according to many commentators, and will help France through any recession. Macron however has resisted German-style Hartz labour flexibility reforms (part of Schroder’s 2010 Agenda).

Hartz reform supporters claim that Germany’s economic growth in the 2000s was largely because of the reforms, which reduced unemployment benefits, removed incentives for early retirement, and increased labour-market flexibility. Opponents claim the reforms had little impact, and that Germany instead.

Whatever its role in strengthening the German economy, the German electorate did not take kindly to the Hartz labour reforms. and replaced the Schroder-led SPD with the Merkel-led CDU. European governments face a similar challenge today. Economies need a new wave of structural reforms, but they are unlikely to be popular in the face of slowing growth. One of the key election-promises of the new Italian government was the removal of labour market reforms by the previous government, designed to increase labour market flexibility. It seems that economic events are set to make European politics even more interesting in 2019.