What you need in a financial advisor will vary depending on your individual circumstances. That being said, there are seven simple rules to follow to find the best financial advisor for you.

1. Know What You Need

You’ve decided you need a financial advisor, but what services do you require from them?

Are you looking to invest wisely, to plan for retirement, or do you need advice on taxes?

Financial advisors offer a wide array of financial services, from investment management through to business finance plans. Only you know exactly the advice you need, but be clear on this before you even begin looking for a financial advisor. The normal financial advisor services are:

Debt Management

Budgeting

Health and long term care planning

Estate planning

Retirement

Inheritance

Tax planning

Investments

Whether you need specific advice on one aspect of your finances or a variety of services, the financial advisor you choose should be able to cover all these areas. Additionally, if you know you’re looking for long-term advice, keep this in mind when choosing.

2. Financial Advising Experience

Frustratingly, nearly anyone can call themselves some kind of financial advisor. It may come under a different heading such as a financial coach or planner, but these titles come with minimum qualifications.

Due to this, it’s important to really know your potential advisor’s experience and qualifications. This ensures your money and assets are in the best hands possible.

A good financial advisor’s website should have their qualifications, education, and experience listed. Review all of these things to figure out whether their knowledge will help your unique needs.

Not all qualifications are equal. In particular, depending on your location, the qualifications to ensure your advisor has are:

The Certified Financial Planner Designation

Certified Public Accountant

Enrolled Agent

Chartered Financial Analyst

Accredited Financial Counsellor

3. Comparing Advisor Fees

It should go without saying that you should do research into different fees for any service. This is never more pertinent advice than with financial advisors.

This is because financial advisors get paid in a few different ways, and sometimes this can be at odds with your best financial interests. For example, if your advisor is getting paid on a fee-only basis regardless of their advice, they have less incentive to grow your wealth. Whereas if they were paid on a commission and fee basis, they have more incentive to invest wisely to increase their commission.

Typically, a financial advisor will be paid one of three ways:

Fee-only

Commission

Fee-based (a mix of both)

You need to figure out what would work best for your individual circumstances.

4. Transparency

While we’re talking fees, it’s time to talk about transparency. Long gone are the days of the elusive and mysterious investment elite. If your financial advisor isn’t being upfront, ditch them.

A good financial advisor will be transparent about all fees to be charged. You should have this in writing, and they should be happy to give it to you.

Not only transparency about fees but also plans. You should be clear on what plans your financial advisor will make, as well as how regularly you can expect updates, reports, and meetings.

5. References and Reviews

Even now, word of mouth might still be one of the best ways to find a financial advisor. But if you don’t happen to know anyone, the internet is a great substitute.

As well as checking qualifications and education, you should check reviews. On their site, on Trustpilot, and on Google.

6. Performance reporting

As we mentioned briefly, you want regular reports on your assets and wealth. But it also needs to be in a digestible format. That is to say, you don’t want an array of random charts and figures you can’t actually understand.

You need clear, concise reports on performance, transactions, and holdings. You can choose how regularly you want to receive these. Whether it’s monthly, quarterly, or bi-annually, your financial advisor should be happy to provide them.

As we live in a digital world, many of these offerings may be in online services. You should know what financial planning software is in use and whether you will have access to it.

7. Talk to Your Advisor

Before signing up for anything, talk to your advisor in depth. If they’re part of a firm, know exactly who will be running your account and who you’ll be dealing with. Get to know them.

Ensure you get an initial meeting – whether by phone or in-person – and know exactly how often you’ll be speaking to them. Is it once a month or once a quarter? Will they regularly be contacting you with updates?

This is particularly important if you’re looking at long-term financial advice. Your life will change due to work, relationships, children, and so on. You need to have regular contact with your financial advisor to take these changes into account and amend your plan accordingly.

Choosing Financial Advisors

Using our tips above, you should be able to find a reliable and trustworthy financial advisor to manage your assets. Make sure to take your time choosing financial advisors, and avoid any cheap pressure tactics from firms.

For more financial advice, make sure to see our financial section to keep you up to date with the latest news.

Even before the coronavirus pandemic, the oil and gas industry was faced with slumping prices. However, with a record collapse in oil demand amid the coronavirus lockdown, the COVID-19 crisis has further shaken the market, causing massive revenue and market cap drops for even the largest oil and gas companies.

According to data presented by StockApps.com, the top five oil and gas companies in the United States lost over $307bn in market capitalization year-over-year, a 45% plunge amid the COVID-19 crisis.

Market Cap Still Below March Levels

Global macroeconomic concerns such as the US-China trade war and the oil overproduction set significant price drops even before the coronavirus outbreak. A standoff between Russia and Saudi Arabia in the first months of 2020 sent prices even lower.

After global oil demand plunged in March, Saudi Arabia proposed a cut in oil production, but Russia refused to cooperate. Saudi Arabia responded by increasing production and cutting prices. Shortly Russia followed by doing the same, causing an over 60% drop in crude oil prices at the beginning of 2020. Although OPEC and Russia agreed to cut oil production levels to stabilize prices a few weeks later, the COVID-19 crisis already hit. Statistics show that oil prices dropped over 40% since the beginning of 2020 and are hovering around $40 a barrel.

Such a sharp fall in oil price triggered a growing wave of oil and gas bankruptcies in the United States and caused a substantial financial hit to the largest gas producers.

In September 2019, the combined market capitalization of the five largest oil and gas producers in the United States amounted to $674.2bn, revealed the Yahoo Finance data. After the Black Monday crash in March, this figure plunged by 45% to $373bn. The following months brought a slight recovery, with the combined market capitalization of the top five US gas producers rising to over $461bn in June.

However, the fourth quarter of the year witnessed a negative trend, with the combined value of their shares falling to $367bn at the beginning of this week, $6.2bn below March levels.

Exon Mobil`s Market Cap Halved in 2020, Almost $155bn Lost YoY

In August, Exxon Mobil Corporation, once the largest publicly traded company globally, was dropped from the Dow Jones industrial average after 92 years. As the largest oil and gas producer in the United States, the company has suffered the most significant market cap drop in 2020.

Statistics indicate the combined value of Exxon Mobil`s shares plunged by 52% year-over-year, falling from almost $300bn in September 2019 to $144bn at the beginning of this week.

Phillips 66, the fourth largest gas producer in the United States by market capitalization, witnessed the second-largest drop in 2020. Statistics show the company`s market cap dipped by 49.6% year-over-year, landing at $22.9bn this week.

The Yahoo Finance data revealed that EOG Resources lost over $21bn in market cap since September 2019, the third-largest drop among the top five US gas producers.

Conoco Phillips witnessed a 42% drop in market capitalization amid the COVID-19 crisis, with the combined value of shares plunging by almost $30bn year-over-year.

Statistics show Chevron witnessed the smallest market cap drop among the top five companies. At the beginning of this week, the combined value of shares of the second-largest US gas producer stood at $141.5bn, a 36.9% plunge year-over-year.

Stock markets are cautiously upbeat that a stimulus package can be agreed in the U.S. before the November 3 election – but even if it does happen, it’s likely to be a “short-lived sticking plaster” that masks the major long-term issue: unemployment.

This is the warning from Nigel Green, CEO and founder of deVere Group, one of the world’s largest independent financial advisory and fintech organizations.

It comes as House Speaker Nancy Pelosi and Secretary Steven Mnuchin spoke again on Tuesday – the deadline imposed by the Speaker – as the two sides try and strike a deal over another significant fiscal stimulus package ahead of the election.

Earlier this month, Republican senators slammed a $1.8 trillion offer made by the Trump administration to the Democrats as too big, an offer Ms Pelosi dismissed as “insufficient.”

Discussions are due to continue on Wednesday upon the Secretary’s return to Washington.

Nigel Green warns: “No doubt, a breakthrough of the deadlock that would allow for more stimulus would provide a lifeline to millions and millions of Americans.

“U.S. and global markets are, generally, cautiously optimistic that a deal can be agreed by the two sides.

“There’s a sentiment that something will have to materialize – and this is fueling markets.

“However, the window of opportunity is closing and it is not yet a done deal.

“If talks collapse, the markets will inevitably be disappointed and there’s likely to be a short-lived sell-off.”

He continues: “Even if Pelosi and Mnuchin can get another massive stimulus package agreed, and U.S. and global markets rise, this is likely to serve only as a sticking plaster.

“A market rally is going to be difficult to be sustained due to the enormous uncertainty created by other factors including the presidential election, a possible looming constitutional crisis in the world’s largest economy, and the growing Covid-19 infections in America and other major economies.”

The deVere CEO goes on to add: “Getting over the political impasse would help boost the economy and deliver much-needed money to Americans, but the major, lasting issue triggered by the pandemic remains: mass unemployment, which will hit demand, growth and investment.

“As such, a swift rebound for the U.S. economy is doubtful as unemployment claims continue to rise.

“That V-shaped recovery talked about by so many? That will be impossible with so many millions facing long-term unemployment.”

Whilst it is certainly positive that unemployment has fallen from 15% in the U.S. to 11% in recent weeks, it should be remembered that this is still at the same rate of the 2008 crash.

In addition, a second wave of soaring unemployment could hit imminently as some support measures wind-down and business’ and households’ savings and resources have been already run-down.

Mr Green concludes: “Near-term support for sure, but a long-term strategy – a multi-year vision – for growth and investment is essential.

“What’s needed is not just more stimulus, but smarter stimulus.”

Excellencies, Ladies and Gentlemen, Esteemed Guests,

It is my distinct honor to welcome you to the UAE’s first-ever digital edition of the Annual Investment Meeting. Thank you to everyone participating, including our panelists from the Governments of Costa Rica, Canada, Nigeria and Russia. Today’s discussion on how countries are ensuring the free flow of trade and investment could not be more timely, especially as the world grapples with the economic recovery and moves toward building a more resilient, post-COVID economy.

As you know, the pandemic has significantly impacted global markets, creating new challenges for trade and investment. According to the United Nations’ 2020 World Investment Report, global FDI flows are estimated to decrease by up to 40% this year, dropping well below their value of $1.54 trillion in 2019. This would bring global FDI below $1 trillion for the first time since 2005. Global FDI flows are expected to decline even further in 2021, by 5% to 10%, and only in 2022 do we expect to start seeing markets recover.

While the challenges ahead are enormous, the UAE sees tremendous opportunity for governments and business leaders to work together through trade and investment to reshape policies, create new partnerships, leverage new technologies, and build a future global economy that is more diverse, inclusive, and sustainable. We know that FDI can bring new technology and know-how, lead to new jobs and growth, and is often the largest source of finance for economies – making today’s discussion even more imperative.

For the UAE, FDI has played a critical role in our economic growth. In 2019, the UAE was the largest recipient of FDI in the region, largely due to our increased focus over the years on enhancing local conditions to attract FDI. With policies and measures in place, such as our Foreign Direct Investment Law enacted in 2018 to further open the UAE market to investors in certain sectors, and the issuance of our Positive List, which allows for greater foreign investment across 122 activities, the UAE was able to increase our FDI value by 32% in 2019. The UAE also came in 16th of 190 countries in the World Bank Ease of Doing Business 2020 Ranking due to our digitization strategies and promising business regulatory environment.

The UAE is continuing to refine and implement policies that will maximize competitiveness, increase collaboration, and provide opportunities to facilitate trade and investment. Our aim is to become the #1 country for foreign investment, target zero contribution from oil to our GDP in the next 50 years, and support research, development, and innovation. The UAE’s trade and investment strategy is centered on economic diversification and focuses on enhanced investment in industries such as communications, Blockchain, artificial intelligence, robotics, and genetics. We are also initiating measures to strengthen our position as a regional leader in supplying financial and logistical services, infrastructure, energy supplies, and other services.

The UAE believes that increased partnership and cooperation with governments and the private sector will be key to achieving our objectives. We view platforms such as the Annual Investment Meeting as instrumental in bridging the gap between nations and supporting global efforts to strengthen international trade and investment. Through this platform, we hope that participants will uncover new, innovative ideas and investment opportunities needed to build back better and ensure a strong post-COVID recovery.

H.E. Dr. Thani Al Zeyoudi, Minister of State for Foreign Trade: Our aim is to become the #1 country for foreign investment, target zero contribution from oil to our GDP in the next 50 years.

Successful Investment Roundtables for Energy and Agriculture concluded with strategies to facilitate sustainable, smart and scalable investments.

Startups took virtual centerstage as they competed at the Global Champions League 2020

AIM Hub

Dubai, October 21, 2020 – After the huge success of its opening day, AIM Digital, the first digital edition of the Annual Investment Meeting, continued to gain momentum as it reached Day 2. The three-day mega digital event, an initiative of the Ministry fo Economy, under the patronage of His Highness Sheikh Mohammed Bin Rashid Al Maktoum, UAE Vice President and Prime Minister and Ruler of Dubai, concluded its second day with interactive activities that catalysed investment-generation, knowledge-enhancement, and local, regional and international collaborations.

Joined by more than 15K participants from over 170 countries, including 70+ high-level dignitaries from across the globe, the second day of AIM Dıgital witnessed a wide range of major events, from the Conference, Exhibition, Investment Roundtables, and Regional Focus sessions to Conglomerate Presentations and Startups competitions; all geared towards providing opportunities to achieve a digital, sustainable & resilient future.

AIM Digital: Virtual Village

In his keynote speech in the FDI session, Ministers Roundtable: Adapting to the New Flow of Trade and Investment, His Excellency Dr. Thani Al Zeyoudi, the UAE Minister of State for Foreign Trade, said: “It is my distinct honor to welcome you to the UAE’s first-ever digital edition of the Annual Investment Meeting. Thank you to everyone participating, including our panelists from the Governments of Costa Rica, Canada, Nigeria and Russia. Today’s discussion on how countries are ensuring the free flow of trade and investment could not be more timely, especially as the world grapples with the economic recovery and moves toward building a more resilient, post-COVID economy. The pandemic has significantly impacted global markets that created new challenges for trade and investment. While the challenges ahead are enormous, the UAE sees tremendous opportunity for governments and business leaders to work together through trade and investment to reshape policies, create new partnerships, leverage new technologies, and build a future global economy that is more diverse, inclusive, and sustainable. We know that FDI can bring new technology and know-how, lead to new jobs and growth, and is often the largest source of finance for economies – making today’s discussion even more imperative.”

He further stated that FDI has played a critical role in the UAE’s economic growth, with policies and measures in place, such as the Foreign Direct Investment Law enacted in 2018 to further open the UAE market to investors in certain sectors, and the issuance of Positive List, which allows for greater foreign investment across 122 activities, and increasing the UAE’s FDI value by 32% in 2019. He also mentioned that the UAE came in 16th of 190 countries in the World Bank Ease of Doing Business 2020 Ranking due to the country’s digitization strategies and promising business regulatory environment.

AIM Digital: Main Registration Page

His Excellency Al Zeyoudi furthered: “The UAE is continuing to refine and implement policies that will maximize competitiveness, increase collaboration, and provide opportunities to facilitate trade and investment. Our aim is to become the #1 country for foreign investment, target zero contribution from oil to our GDP in the next 50 years, and support research, development, and innovation. The UAE’s trade and investment strategy is centered on economic diversification and focuses on enhanced investment in industries such as communications, Blockchain, artificial intelligence, robotics, and genetics. We are also initiating measures to strengthen our position as a regional leader in supplying financial and logistical services, infrastructure, energy supplies, and other services.”

He added: “The UAE believes that increased partnership and cooperation with governments and the private sector will be key to achieving our objectives. We view platforms such as the Annual Investment Meeting as instrumental in bridging the gap between nations and supporting global efforts to strengthen international trade and investment. Through this platform, we hope that participants will uncover new, innovative ideas and investment opportunities needed to build back better and ensure a strong post-COVID recovery.”

Furthermore, world-class speakers shared their viewpoints in Day 2 of the Conference highlighting Foreign Direct Investment, Foreign Portfolio Investment, Small and Medium-sized Enterprises, Startups, Future Cities, and One Belt, One Road, including H.E. Amb. Mariam Yalwaji Katagum, Minister of State, Federal Ministry of Industry Trade and Investment of The Federal Republic of Nigeria; Victoria Hernández Mora, Ministry of Economy, Industry and Commerce of Republic of Costa Rica; Hon. Victor Fedeli, Minister of Economic Development, Job Creation and Trade of Ontario, Canada; and Sergey Cheremin, Minister of Moscow City Government Head of Department for External Economic and International Relations, among others.

Two Investment Roundtables were also held successfully at the second day of AIM Digital, concluding with strategies to facilitate sustainable, smart and scalable investments. The Energy Roundtable was led by Laszlo Varro, the Chief Economist of International Energy Agency, which works with countries around the globe to structure energy policies towards a secure and sustainable future. Among the notable participants include H.E. Arifin Tasrif, Minister for Energy & Mineral Resources of the Republic of Indonesia; and H.E. Gabriel Obiang, the Minister of Mines and Hydrocarbons of Equatorial Guinea. The Agriculture Roundtable was led by Islamic Development Bank Group, the multilateral development bank working to promote social and economic development in Member countries and Muslim communities worldwide, delivering impact at scale.

In addition, the second set of National Winners competed on Day 2 of the AIM Global National Champions League. Overall, a total of 65 countries competed at this international startups competition. The top five global champions that will win a total prize of USD50,000 will be announced on the last day of AIM Digital. The competition was launched in a bid to help startups in maximizing their potential to attract funding and promote their business ideas to a global audience, getting utmost exposure and expanding their network.

Participating in the Conglomerate Presentation feature of AIM Digital is Elsewedy Electric led by Eng. Ahmed Elsewedy, its President and CEO. Elsewedy Electric began as a manufacturer of electrical components in Egypt 80 years ago, and Electric has evolved into a global provider of energy, digital and infrastructure solutions with a turnover of EGP 46.6 billion in 2019, operating in five key business sectors, namely Wire & Cable, Electrical Products, Engineering & Construction, Smart Infrastructure and Infrastructure Investments. As part of its commitment to sustainability, it has established green energy and smart metering projects across Africa, the Middle East and Eastern Europe.

AIM Digital: Exhibition Booth

The Regional Focus Sessions featured the regions of Asia and Latin America and explored the risks, challenges and opportunities for growth and regional cooperation. Regional Focus Session on Asia brought together government officials and investment authorities from the ASEAN Member States and discussed their strategies to create a borderless and sustainable bloc that will push organic growth, as well as their approaches to gain resilience in the economy. Regional Focus Session on Latin America highlighted the significance of regional and international partnerships to combat the current pandemic and boost trade, investments and employment within the region.

Moreover, Country Presentations on Day 2 presented the outstanding features and investment opportunities in Colombia, Egypt and the Federal Democratic Republic of Ethiopia which highlighted the countries’ status as attractive investment destinations.

Another highly anticipated event in the largest virtual gathering of the global investment community is the announcement of winners for the Investment Awards and Future Cities Awards which will take place on Day 3 of AIM Digital. AIM Investment Awards will grant recognition to the world’s best Investment Promotion Agencies and the best FDI projects in each region of the globe that have contributed to the economic growth and development of their markets. Likewise, AIM Future Cities Awards will give tribute to the best smart city solutions providers and for outstanding projects that have resulted to enhanced operational efficiency and productivity, sustainability, and economic growth.

Day 1 of AIM Dıgital welcomed the presence of globally renowned personalities such as the UAE Minister of Economy, His Excellency Abdullah bin Touq Al Marri who emphasised the vision of UAE’s wise leadership for the post-COVID era, reflecting great significance to enhancing the readiness of the country’s government sector, raising efficiencies and performance at the federal and local levels. Keynote remarks were delivered by H.E. Juri Ratas, the Prime Minister of Republic of Estonia; H.E. Rustam Minnikhanov, the President of the Republic of Tatarstan; H.E. Dr. Bandar M. H. Hajjar, the President of Islamic Development Bank Group (IsDB Group); H.E. Mohammed Ali Al Shorafa Al Hammadi, the Chairman of Abu Dhabi Department of Economic Development (ADDED); and Dr. Mukhisa Kituyi, the Secretary-General of the United Nations Conference on Trade and Development (UNCTAD).

AIM Digital: Virtual Lobby

The UAE Minister of State for Entrepreneurship and SMEs, His Excellency Dr. Ahmad Belhoul Al Falasi, underlined in his Keynote Address for the SME Pillar, that it is crucial for Startups and SMEs to be given opportunities to bounce back from the impact of pandemic and provide a conducive environment that will empower them to have the capability of supporting growth and success.

The Global Leaders Debate featured prominent keynote debaters such as Armida Salsiah Alisjahbana, the Under-Secretary-General of the United Nations and Executive Secretary of United Nations Economic and Social Commission for Asia and the Pacific (UNESCAP); Mohamed Alabbar, the Founder of Emaar Properties, Alabbar Enterprises and Noon.com; Mohammad Abdullah Abunayyan, the Chairman of ACWA Power; and Arkady Dvorkovich, the Chairman of Skolkovo Foundation, who discussed the strategies to restructure the economies in overcoming the consequences of the pandemic.

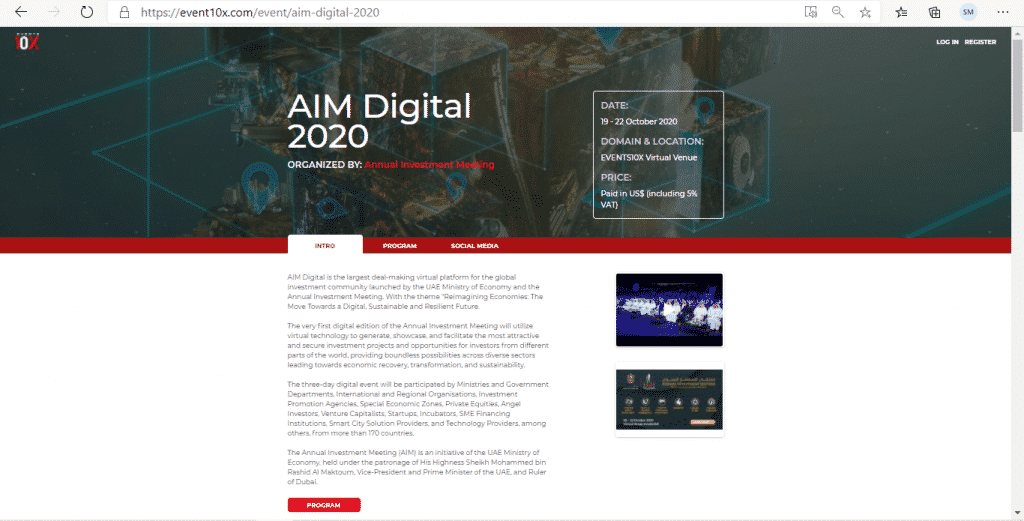

The first digital edition of the Annual Investment Meeting with the theme “Reimagining Economies: The Move Towards a Digital, Sustainable and Resilient Future, will be held until the 22nd of October 2020.

The Annual Investment Meeting (AIM) is an initiative of the UAE Ministry of Economy, held under the patronage of His Highness Sheikh Mohammed bin Rashid Al Maktoum, Vice-President and Prime Minister of the UAE, and Ruler of Dubai. AIM is the world’s leading investment platform with over 16,000 participants coming from more than 140 countries. Over 400 exhibitors and co-exhibitors, 60+ high-level dignitaries, 150+ investment specialists and experts have participated in AIM 2019.

Plenty of people feel out of their depth when it comes to money management. Whether you’re looking at pensions, insurance, mortgages, or savings and investment products, there are so many options available and it can be overwhelming. Recent research has shown that up to one-third of people in the UK don’t have a pension. It’s really critical to plan for the future and many people could benefit from professional financial advice. The benefits of a financial adviser include bespoke advice on defining your financial goals, building wealth, and planning for the future.

Read on to find out more about the value of good financial advice.

7 Benefits of a Financial Adviser

A good financial adviser will begin the process of working with you by undertaking a fact-finding exercise. They will find out more information about your circumstances and goals and any financial products you already have.

One of the most important things is to assess your risk appetite. How much are you prepared to lose in the investment market? Once all of this is established, they will go on to recommend financial products that are suitable and affordable for your current circumstances.

Let’s look in a little more detail about the specialist advice available from financial advisers.

1. Product Recommendations and Protection

If you take financial advice before buying a specific product, you should end up with a product that meets your personal needs and is most suitable for your circumstances. Using an adviser may also give you access to a range of products that you may not have been able to access on your own.

You also have protection if something goes wrong. If your adviser gives unsuitable advice or has not acted in your best interests, you can complain to the Financial Ombudsman.

2. Objective, Expert Advice

Lack of objectivity can be a major issue in investment decisions. A professional adviser will make their decisions based on analysis and objective decision-making, without emotion or panic. An experienced professional will know when to hold their nerve if the market looks a little shaky, enabling sound long-term decisions.

Financial advisers are full-time professionals with many years’ experience. No matter how hard you try, it’s hard to keep up-to-date on all the latest developments in taxation, investment opportunities, and market developments. You should be able to rely on your financial adviser to give you the most well-informed advice.

3. Savings Advice

Let’s look at some of the areas where financial advisers can add value to your decision-making process. In terms of savings advice, it’s easy to get general guidance on what your savings options are. Financial advisers will go further and offer advice on particular products.

A financial adviser would take you through specific options of savings accounts, ISAs and investment opportunities, and recommend one that suits your personal circumstances best.

4. Investment Advice

It’s important to note that some financial advisers are independent and offer a full range of products from the market. Others offer a more restricted service and only have a limited range of products or providers.

Investment products are harder to understand than cash savings products, and taking advice can ensure that you’re aware of all the options available to you. If you have limited time to undertake research, or you lack the skills and knowledge to make the best decisions when it comes to investing, then financial advice in this area is a good idea.

5. Long-Term Financial Planning

A key part of getting your personal finances in order is ensuring that you plan for the future. Pensions are long-term investments and it’s important to understand the funds you’re investing in and any associated risks.

A financial adviser can help you to make decisions about personal pension products or boost your existing pension. If you’re considering combining different pension pots, it’s important to get expert advice so that you are fully informed on how each product works and what plan is most suitable for your long-term financial security.

6. General Money Management Advice

A good financial planner can also help you with general finance tips. This could include how much you need to save in your emergency fund and what your long-term savings target should be. They can also help with budgeting tips – what do you need to do differently to improve your financial circumstances?

Financial advisers can offer banking advice to make sure that your current bank is offering the services you require. This could include looking at bank charges including overdraft fees, the availability of digital and face-to-face services and any additional services offered with your bank account.

Financial advisers can also help to identify any changes you could make to improve your tax situation. This includes long-term tax and estate management planning, as well as any tax implications from investments.

7. Peace of Mind

Possibly the greatest benefit of using a financial adviser is that it gives you peace of mind. You can relax, knowing that your money is in a safe place and that your financial adviser will help you to deal with any challenges which may arise.

You can also feel secure in the knowledge that, should your life circumstances change, your financial adviser ill be able to help you navigate through the transition. This will reduce stress and help you to continue on your path towards financial freedom.

Choosing a Financial Adviser

If you’re now sold on the benefits of a financial adviser, the next step is to choose one. You need to ensure that you fully understand their fee structure. Some charge by the hour, while others charge a flat fee for a specific product or take a commission on products that you buy through them.

You should also ensure that the financial adviser you use is fully qualified and registered with the Financial Conduct Authority. This means that they meet the required standards and also that you have some protection if you’re unhappy with the service provided.

Staying Informed

Even with the benefits of a financial adviser to help you make financial decisions, it’s a good idea to try to stay as well-informed as possible about what’s going on in the finance world.

For all the latest news and views on investments, banking, and finance, be sure to check out our blog.

The 10-day virtual event will offer exhibitors a cost-effective platform to showcase their best projects, expand their business network and grow globally.

Dubai, (September 7, 2020) – The International Property Show, in partnership with Invest in Dubai (IID) Real Estate, is absolutely primed for a remarkable world-class virtual exhibition that will offer a wide array of lucrative opportunities and a one-of-a-kind immersive experience to exhibitors from across the globe.

From the 11th to 20th of November, the real estate industry’s largest virtual exhibition with more than 20K participants from over 40 participating countries, will gather leading real estate developers, top-tier investors, industry experts, and professionals, in a secure virtual platform to leverage business opportunities and attract major investors from local, regional and international real estate markets.

“The powerful collaboration between the International Property Show and Invest in Dubai is a massive opportunity for exhibitors to promote and boost their brand and be exposed to a vast network of investors from around the world. Exhibitors will not need to worry about visitors coming to their stand because the whole world can visit them through virtual technology. With the use of technology, we are shaping the way the real estate market functions and are making it easier to bring together the entire global real estate community,” stated Mr. Dawood Al Shezawi, the President of the organizing committee of the International Property Show.

A multitude of advantages await the exhibitors of the first virtual edition of the International Property Show. As a globally acclaimed property exhibition, the virtual platform offers exhibitors a maximum exposure to 20,000+ high-quality visitors locally and internationally, gaining a greater opportunity to generate leads and boost sales without the added travel and accommodation expenses. Every exhibitor will have their exclusive virtual slot where they can showcase their projects as well as their expertise and competitive edge in the market.

“Dubai has embarked on a successful journey to incorporate innovation digitalization across all sectors and to create solutions that positively influence the productivity of the real estate industry. In addition to this, international markets are also utilising innovation in order to be resilient and bounce back from the impacts of pandemic. Likewise, through this strong collaboration, technology will be instrumental for exhibitors to have the virtual gateway to access new opportunities such as the increased promotion and sales of their various projects, creation of long-lasting relations and formation of rewarding collaborations and partnerships, which can all be achieved in the comfort of their own homes,” asserted Mr. Al Shezawi.

Exhibitors are also given the special privilege of utilising the different virtual activities of IPS Aside from having their own Virtual Exhibition Space, exhibitors will be able to get free access to Webinars and will have the chance to be a part of the panel discussions, together with other industry experts and specialists, giving them more exposure and bigger opportunity to build their reputation and boost their organization.

Via the virtual venue hosted by Events10X, exhibitors can present their projects through advanced technology by taking part in Project Presentations. They also gain the chance to meet esteemed local and international Media Specialists, in the Meet and Greet feature, one of the interactive virtual activities of the event. Moreover, exhibitors will experience fast, seamless and secure transactions as they negotiate with serious buyers and close deals in a safe and secure virtual platform that fully protects their privacy.

In partnership with IID, this major event also serves as an ideal platform for local developers to showcase their most outstanding projects in Dubai and play a major role in promoting the city as a global investment destination, prompting more opportunities for growth within the Dubai real estate sector.

“It is a great honour to host the IPS alongside IID as exhibitors and visitors are offered a superior platform to connect with like-minded individuals. Through this event, we would like to satisfy the collective needs within this rapidly changing real estate industry and also boost investments in Dubai and in other parts of the world through technological advancement. Being a consistently successful event for many years now, we view the pandemic as a great opportunity to realise our true potential and create greater flexibility for every organisation in the industry,” added Mr. Al Shezawi.

Overspending on a holiday is a very easy trap to fall into. The excitement of being in a new place, seeing sights, and eating new food can quickly total up. However, you can do all of these things without going over your budget. By implementing a few ideas, you can make sure your holiday is not ruined by money and cash worries. Below, we discuss our tips for holiday budgeting.

Be Flexible

When booking transport and accommodation, you can save a lot of money if you are able to be flexible. Flights and train tickets can drop drastically if you can shift around days and times. Trains are much cheaper if you travel off-peak and book well in advance.

Try to utilize price comparison sites. They can get you the best deals on flights and accommodation and often have offers available.

Luggage

Luggage can really add money to a flight, particularly when flying with budget airlines. Most of their prices are advertised without hold luggage and strict hand luggage restrictions apply.

Use this to your advantage by only booking the number of cases needed. If you and your partner can fit the children’s clothes in two cases, then you can save money on expensive hold luggage places.

If you are traveling somewhere for a longer period of time, it can be cheaper to send clothing via post than book extra hold luggage. Look at parcel comparison sites using the dimensions and weight of your package and send them to your destination.

Plan for ATM Withdrawals

When withdrawing money from abroad, prices can vary drastically. There are three factors to consider; ATM fee, bank fee, and exchange rate.

The ATM fee is the money charged by the ATM operator for the use of their machine. These fees can vary from free services to extortionate prices. Ask locals in the area which are the free ATM machines and use them.

You should also check the bank exchange rates from your currency to the local currency. Most bank ATM machines will have fairly reasonable exchange rates, but independent ATM operators can charge high fees.

Next, consider the charge that your own bank makes for taking money out abroad. To minimize a loss on all counts, always keep ATM withdrawals to a minimum, withdrawing as much money as you possibly can to maximize your loss.

Holiday Budgeting

Before the holiday starts, count up the money you have saved. Deduct any money for transport or hotels, then divide the rest by the number of days you will be away. You now have a daily budget for your trip.

If you do not spend all of your holiday budget in one day, then carry it over to the next. However, try not to exceed your budget on any given day as it can be hard to make up the losses. You may want to also have a separate budget for buying gifts and souvenirs that runs for the whole trip.

Budget for Time

Arrange your personal finances around your times. For example, you may be spending one day on a flight which will cost you far less than a day in a city. For every day like this, carry your daily budget over to the next.

If you find yourself spending more money than you planned, slow the trip down a little. Instead of going out every day, spend a few days by the pool. You may decide to cook in an apartment instead of going out for expensive meals or eat food from a street vendor.

Pay Using Card

When paying by card in a shop or bar, always choose to pay in local currency. Paying in your own currency usually has a higher rate with conversions fees, so you will end up being charged more. When using a credit card, the rate will be set by Visa or Mastercard and will likely be much lower.

Research Local Deals

Before you travel to a destination, do some research online for local deals and offers. These may be in the form of discount coupons for trips and sights, or for meals and food.

Many restaurants have excellent tourist meals for visitors. You can save a lot of money, eating at very high-end restaurants in this way. Check local review sites for great places to eat then check their website to see what they offer.

Create Your Own Tours

Arranged tours and guides are very useful. But they can also be very expensive. Save money by planning your own itinerary.

If you are the adventuring type, get online, and utilize public transport. You may even hire a car or bicycle to go and see the sights. The joy of this is that you see a lot more of the destination and often find shops, food, and sights you would not have been exposed to before.

Some city breaks even offer free walking tours. They are organized by knowledgeable guides who ask for a contribution at the end. You simply pay what you think they deserve and have worked for.

Some destinations also offer combined travel and discount cards. They allow you access to transport and discount at major attractions and eateries. Family tickets can save you an awful lot of money in the long run.

Coming Home

When you return, exchange any large amounts of leftover currency at ane exchange. For medium amounts, it may worth be worth the effort so it could be better to just spend them at the airport on your way home.

If you are looking for more advice on holiday budgeting or general money management, then make a visit to our blog a regular stop. Whether it is personal or business finance advice, we can help you organized your money starting today!

A disputed result in November’s U.S. presidential election is now the number one concern for investors – even ahead of a second wave of Covid-19 – according to a new global survey.

The poll carried out by deVere Group, one of the world’s largest independent financial advisory and fintech organizations, asked more than 700 clients ‘What is your biggest investment worry for the rest of 2020?’

A contested U.S. election was the number one (72%); the impact of a Covid-19 second wave (18%) and U.S.-China trade war (5%). The remaining 5% was made up of other geopolitical issues, including Brexit.

735 people resident in the UK, North America, Europe, Asia, Africa, Latin America and Australasia took part in the poll.

Of the poll’s findings, deVere Group CEO and founder, Nigel Green says: “Investors around the world are beginning to freak about the U.S. presidential election.

“But not about whether Trump or Biden wins, rather over the looming possibility of a disputed outcome.

“President Trump is already questioning the legitimacy of the election, heightening the chances of a contested result and an ensuing constitutional crisis in the world’s largest economy.

“It’s getting ugly and investors are, rightly, concerned that this will generate massive waves of volatility in the markets, not only in the U.S., but around the world.”

He continues: “Investors are telling us this is their biggest investment worry for the rest of 2020.

“It is likely that any election-triggered volatility will be highly impactful for may be only two or three weeks.

“As always, investors should remain in the market during this time.”

Rational investors, Mr Green believes, should be capitalising on any election turbulence.

“There are two key reasons why investors should be building up their portfolios in volatile times.

“First, are long-term benefits. There are many unknowns, but what we do know is that over the longer-term the performance of stock markets is fairly predictable: they go up.

“Indeed, for this reason, over a longer time horizon, investing in equities is almost universally recognised as one of the best ways people can accumulate wealth.

“By not topping up and diversifying portfolios in volatile periods, investors are pushing back the longer-term benefits they could be starting to reap. Why forsake the long-term gains that would be generated on money invested now?”

“Second, the buying opportunities. The see-sawing markets are a chance for investors to put new money into markets at lower prices. A slump in the market means that there are high-quality equities available at more attractive prices.”

The deVere CEO concludes: “A contested outcome of the U.S. presidential election will almost inevitably send the stock markets into a temporary tailspin – and this is weighing on investors’ minds.

“I would argue, they should try and use the volatility to their financial advantage where possible and appropriate.”

The American economy has millions of people working paycheck to paycheck. As if it’s not enough, 80% of Americans are walking around with some type of debt to keep their head over water as a way to afford bills or pay back tuition looking for ways to reduce debt.

Debt also happens to those who have a poor understanding of finances or those who desire to meet a certain lifestyle. It can be exhausting to try to pay back what you owe when it is a lot. If you need tips on how to reduce debt and get back on track, keep reading.

1. Learn Where You Stand

There are two types of debt a person who owes money has: problem debt and managed debt. When you are riddled with debt uncertain of how to pay it back, you are dealing with problem debt. This is because you are in a position where you take out more than what you can afford.

The goal is to turn problem debt into managed debt so you can work to pay it back to be debt-free. This cannot happen if you do not know where you stand. The best way to be clear about your financial situation is to pull out a pen, paper, and your credit report.

Your report will provide you a list of credit cards and loans you have, how much you owe, and whether or not you are current on the payments or not. If there happen to be discrepancies on your report, now is the time to correct it.

2. Budget and Start a Debt Plan

Before you contact lenders, you should create a debt management plan and create a budget to see what you can afford to pay. You may be able to pay more than you think each month if you can cut out certain expenses you do not need such as shopping.

If you are able, you could also increase your budget by working more hours or finding another job. You can do this by yourself or you can work with a financial consultant to help add structure to your plans and guide you.

3. Pay off Debt With the Avalanche or Snowball Method

You are in better control of your personal finances when you can order how, how much, and when you repay money you owe. There are two types of debts you may have. The first, known as revolving debt, comes from credit cards that have a monthly balance each month when you do not pay it back (in full).

There is also installment debt that is a chunk of money you owe at once — although you pay back in installments. This is the case with mortgages, personal loans. Both can affect your credit score. It’s helpful to use the avalanche or snowball method when you are paying your debt back.

Avalanche Method

With this method, you pay off debt from the highest interest to the lowest. Overall, you want to make at least the minimum payment, but add more money to accounts with higher interest. You continue this process to the end and doing this method helps you decrease the total amount of money you owe by reducing the interest.

Snowball Method

With the snowball method, you are doing the opposite. You are paying back from smallest to largest. This method also works to lower the amount of debt you owe, but by eliminating debt which stops interest.

4. Negotiate to Settle

If you do have some money on the side or can get it, you may be able to clear the debt you owe quicker by settling on the balance with a lender. With this method, you are paying less than what you owe on the balance that the lender accepts.

This amount may be as little as 20% or as much as 80% to 90% off your balance. The only way to figure out how much you can get off is through negotiation. Upon receiving your payment, they will show your account as paid.

5. Consolidate Debt

Another option to address debt is to consolidate it. A major benefit is that it can help with your credit scores. When you consolidate debt, you are rolling all your debt, including the interest rates, into one single payment and interest.

The attractive thing about debt consolidation is that you save more by having a reduction in interest so you can pay back the money you owe faster. This method is also ideal for those who find it hard to keep up with multiple payments.

6.Do Not Add On to Debt

The last thing you want to do as you are working to repay debt is to add on to it. You should never attempt to get another loan or card to pay an existing debt. More often than not, this will make matters worse and it will be more difficult.

This also means you need to change old habits that caused you to get in debt in the first place if you have problems spending. A good tip to avoid getting in more debt is to stop using credit cards when shopping and switch to cash when you know you cannot pay the balance back in full. Relearning to use cash rather than depending on credit cards can make a huge difference.

Reduce Debt to Get Back on Track With Your Finances

When you first get a credit card or loan, it can be an exciting feeling. It feels nice to be able to get something you want or pay a bill you previously could not afford to pay back. Every time you use money from a lender, you should always keep in mind the money is not yours, and it comes with interest.

When you do not pay what you owe, you will find it hard to get future approvals and notice a plunge in your credit score. There is a way to reduce debt and get rid of it when you acknowledge you have it and use the tips to get ahead of your finances.

If you want to find more ways to keep your money in check, take a look at more blogs on the finances section on our website.