Having reached almost every country across the globe, the social and economic side-effects of the COVID-19 pandemic took root in national economies and businesses of all sizes, as seismic change, tumbling stock markets and rising unemployment necessitated a greater need for rapid response solutions across the globe.

Data from the period between October 2020 and January 2021 (against pre-pandemic levels) showed that a quarter of companies saw sales drop by 50%, although despite the initial impact, many firms managed to retain workers (around 65%) through reducing wages, hours or by granting leave, resulting in only 11% of companies laying off workers (Worldbank).

Opening Up

Partway through 2020, the Asia Foundation asked owners of MSMEs as to how they were able to navigate the pandemic while staying afloat. At the time, over half of all MSMEs in Thailand, Lao

PDR, Malaysia, and Timor-Leste had either shut down completely or were closed to customers, with Malaysian MSMEs being hit hardest (with just 5% of businesses running as “normal”).

With Malaysian COVID-19 cases still fluctuating, the country is now open for business, albeit tentatively. With disruption to travel still prevalent across the globe and a notable absence of overseas guests, Malaysia’s normally-flourishing hospitality industry has slowed considerably.

Staying Afloat

Other business types have fared better: at the outset of the pandemic, micro, small and medium-sized enterprises (MSMEs) across South East Asia were relatively quick to respond. Representing between 97% and 99% of all firms and between 60% and 80% of total employment, smaller businesses were able to demonstrate a greater degree of resilience, flexibility and responsiveness, due in part to their size.

However, despite relative success in reducing public health risk throughout 2020, lockdowns had a major impact on households and small businesses alike. Many MSMES reported revenue losses of over 50% by comparison to levels prior to Covid. As with other brick and mortar outlets, low customer traffic led to closures (some permanently). Those which remained open received significantly reduced footfall, with additional limitations due to reduced pay and changes in working conditions.

Moving Forward

In response to the economic crisis, Southeast Asian governments responded by producing a series of programmes to support those most affected by the widespread disruption, including schemes offering financial support (primarily to small businesses). However, as the Asia Foundation reports, in hindsight these could have been optimized to be more effective.

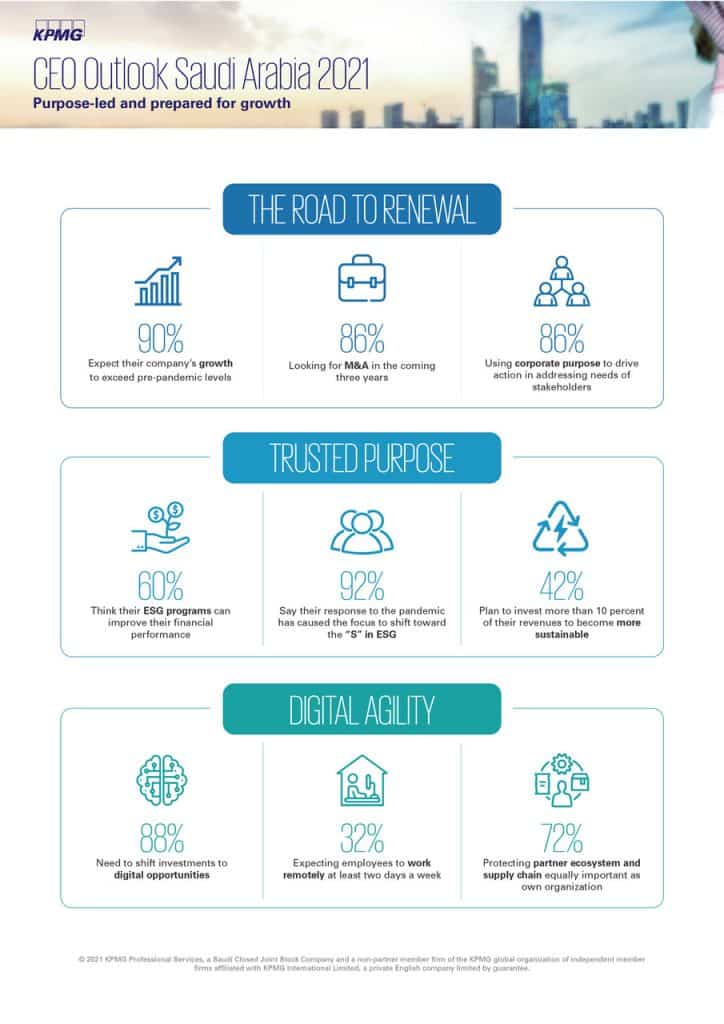

KPMG outlines four stages on the path to recovery for businesses worldwide: the ability to react quickly, resilience, recovery plans and the capacity to adapt to a changing “new reality.” In addition to government support offering tax-relief holidays and subsidies, lessons learned during previous waves can potentially be used to develop more effective future programmes.

Steps Towards Recovery

From a business perspective, there are three key ways to approach the current crisis. Firstly, a collaborative approach offers benefits to both parties,helping to increase both the reach and impact of two businesses working alongside each other.

Secondly, organizational agility is now viewed as essential to all businesses. Through formulating contingency plans and by preparing to deal with unknowns, businesses are better equipped to steel themselves against further closures. Finally, digitalization can be an effective way to create additional flexibility, though it is not by any means a complete solution in and of itself.

If you are considering a career shift towards a role in the business sector, studying an MBA Online in your chosen business specialty field can help guide you towards the job you want.