The Islamic Development Bank (IsDB) Group hosted a webinar on the impact of the COVID-19 pandemic on the global investment outlook, which was organized in collaboration between the United Nations Conference on Trade and Development (UNCTAD) and the Country Strategy and Cooperation (CSC) Department, IsDB on 17th November 2020 to discuss the impact of COVID-19 on FDI and trade in OIC member countries.

The main objective of the webinar is to present the key findings of the World Investment Report 2020 – International Production Beyond the Pandemic with a highlight on FDI trends in foreign direct investment (FDI) worldwide, at the regional and country levels and emerging measures to improve its contribution to development. In addition to presenting IsDB Group Strategy during COVID-19 and its impact on OIC Member Countries and Investment Promotion Agencies (IPAs).

The Webinar also proposed adopting policies and strategies to revive investment and trade in member states to advance investment promotion activities, in order to support the IsDB Group efforts to assist Investment Promotion Agencies (IPAs) in member countries by assisting them in devising appropriate investment and trade policy responses to the ongoing pandemic

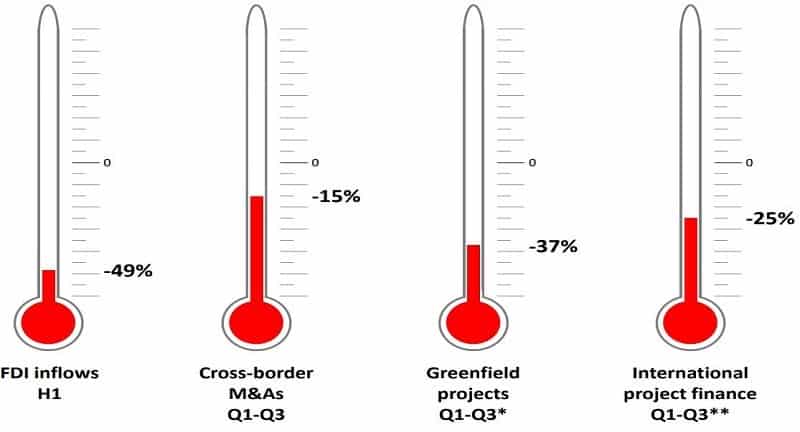

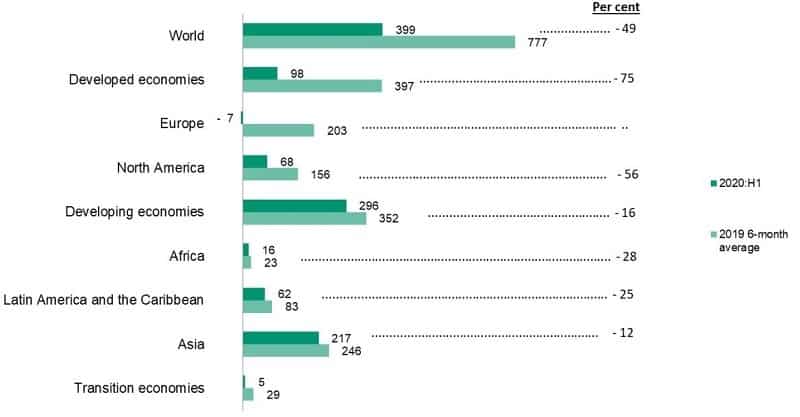

Mr. Oussama Kaissi, CEO of the Islamic Corporation for the Insurance of Investment and Export Credit (ICIEC), stated that “the COVID-19 pandemic has created a devastating global health crisis. According to UNCTAD’s 2020 World Investment Report, global flows of foreign direct investment (FDI) will be under acute pressure this year as a direct result of the pandemic. In order to combat these implications in member countries, IsDB and its group members have implemented a number of initiatives to maintain trade and investment flows. ICIEC will be an important part of the long-term recovery, supporting the growing demand for risk mitigation solutions”.

Mr. James Zhan, Director, Investment & Enterprise Division, UNCTAD, made a presentation which highlighted the key findings and policy recommendations found in its World Investment Report 2020: International Production Beyond the Pandemic.

Mr. Amadou Diallo, the Acting Director-General, Global Practices at the Islamic Development Bank in his speech stated that during COVID-19, the Bank provided technical assistance programs for the Islamic Development Bank Group such as RCI and ITAP to support the Member Countries by assisting them in developing suitable plans for investment and trade policy to confront the ongoing Corona pandemic. This is in the framework of a tripartite approach centered around the “response, recovery and rebuilding” pillars.

Mr. Mohammed Bukhari, Senior Investment Promotion & Regional Cooperation Specialist, CSC Dept., IsDB delivered a presentation on the impact of COVID-19 on MCs, particularly in foreign direct investment (FDI), domestic investment and investment promotion agencies (IPAs).

It is noteworthy that the private sector institutions of the Islamic Development Bank Group played an important role during COVID-19, as Mr. Asheque Moyeed, Division Head, Infrastructure & Corporate Finance, the Islamic Corporation for the Development of the Private Sector (ICD) made a presentation which focused on the efforts related to promoting investment in member countries, where the IsDB Group private sector institutions pledged with IsDB to provide $ 700 million to stimulate investment, finance trade, investment insurance and export credit in member countries. Two D-8 Egypt and Turkey are going to utilize around $270 million of this package.

The webinar brought together over 500+ participants from 113 countries, including government officials, Presidents & CEOs of local/international private sector companies, multilateral and financial institutions, individual investors, entrepreneurs, chambers of commerce & Industry, business associations, and investment promotion agencies