This is a retired estate. blog.cfi.co was published between 2019 and 2026, largely outside CFI.co’s editorial process: much of it was templated, and part of it was supplied through a third-party content agency’s account. It also carried republished CFI.co editorial material. It is not governed by the CFI.co governance file and it is not part of CFI.co’s hashed public archive. Publishing here stopped on 30 July 2026.

193 links across 139 posts on this subdomain were commercial placements and carried no disclosure at the time. In July 2026 each link was marked. This notice is the disclosure; the posts do not carry individual dated notes. Nothing has been deleted or unpublished: every page remains at its original address.

Also: Seeking Alpha, TheStreet.com, Capital Finance International

All economies affected by the pandemic have something in common. The rate of vaccination of the population—quite different in different countries—has been the main factor determining the prospects for the resumption of economic activity, as it is a race against local waves of transmission of the virus.

Personal contact-intensive services have borne the economic brunt of the pandemic. To the extent that vaccination enables them to restart, one may even be able to witness some temporary dynamism in the sector because of pent-up demand. However, international tourism will not be included at the outset since vaccination will have to reach an advanced level both at the origin and destination of travelers.

But let us not be deceived: the pandemic will leave scars and countries will not return to where they were. There will be a need for retraining and job reallocation for part of the populations of all countries.

The pandemic is leaving a trail of unemployment, particularly affecting minorities, low-skilled workers and, in Emerging Market and Developing Economies, women, who predominantly occupy jobs in contact-intensive services. Figure 1 displays estimates presented in chapter 4 of the IMF April World Economic Outlook released on March 31.

Before the pandemic, it was already known that ongoing technological changes—automation and digitalization—were posing challenges in terms of the need for training or retraining for part of the workforce. Well then! The response of companies and consumers to the pandemic has deepened these trends and is not expected to be entirely reversed.

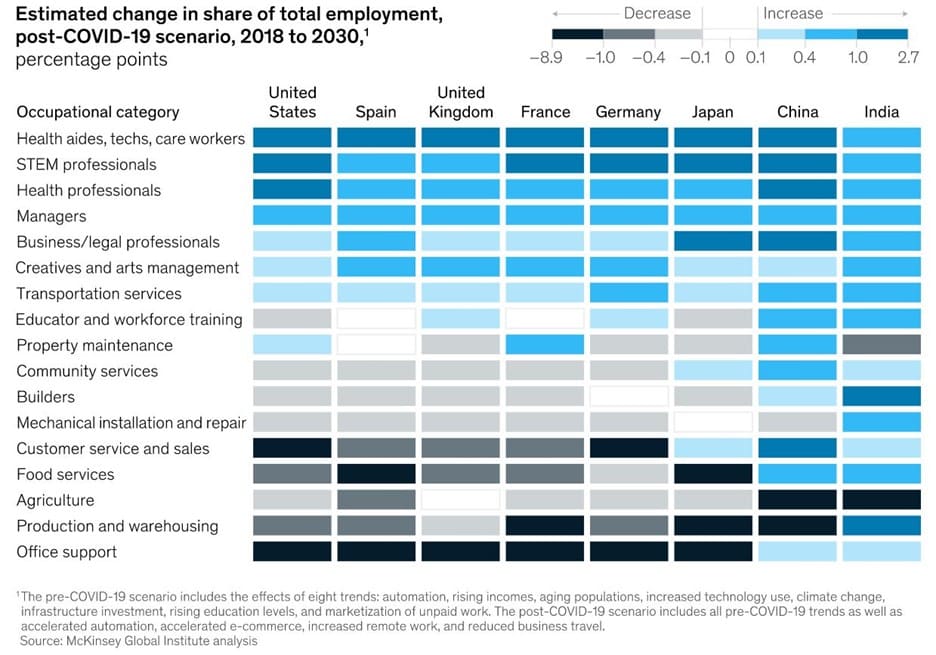

A February 2021 report by the McKinsey Global Institute estimated that in eight countries (China, France, Germany, India, Japan, Spain, the United Kingdom and the United States), more than 100 million workers will have to find new, more qualified jobs by 2030. This is 25% more than they had previously projected for developed countries. Figure 2 shows their estimates of shifts in occupations by 2030, with a relative rise in healthcare and science, technology, engineering, and mathematics (STEM), while jobs in food service and customer sales and service roles decline. Less-skilled office support roles would also tend to shrink.

Why? Many of the practices adopted during the pandemic are likely to persist. Where done, consumer surveys indicate that sales via e-commerce, which have grown substantially during the crisis, are not expected to shrink too much. Also, remote work will not be fully reversed, with the hybrid organization of work processes becoming more common. The fact that employees in remote occupations have worked more hours and with greater productivity during the pandemic will encourage continued telework.

McKinsey suggests that changes in “work geography” will have consequences for urban centers and workers employed in services, including restaurants, hotels, shops, and building services—25% of jobs in the United States before the pandemic, according to David Autor and Elisabeth Reynolds (The Nature of Work after the COVID Crisis: Too Few Low-Wage Jobs; July 2020). Indeed, demand for local services in cities has dropped dramatically as remote work has increased, regardless of confinement.

Autor and Reynolds indicated four trends for the world of work after the pandemic. In addition to automation, they highlighted the increase in remote work, the reduction of density of workplaces in urban centers, and business consolidation. The latter is due to the growing dominance of large firms in many sectors, something exacerbated by the bankruptcies of smaller and more vulnerable companies.

All these trends have negative impacts on low-income earners and the distribution of income. They tend to increase the efficiency of processes in the long run, however, leading to harsh consequences in the short and medium terms for workers in personal services, who are generally not present among the highest paid. Workers at the top of the wage pyramid, including professionals in STEM, will see their opportunities grow.

Technological progress is one of the main causes of the increase in income inequality in advanced countries since the 1990s. The acceleration of inequality with the pandemic therefore tends to intensify the challenges. In a way, it can be said that the pandemic is accelerating history, rather than changing it.

The role of public policies will be central in the post-COVID-19 world, both in strengthening social protection—including through unemployment insurance and income transfer programs—and in the requalification of workers. Instead of denying technological advancement, it is better that public authorities help people to adapt, minimizing the resulting scarring.

Otaviano Canuto, based in Washington, D.C, is a senior fellow at the Policy Center for the New South, a nonresident senior fellow at Brookings Institution, an adjunct assistant professor at SIPA – Columbia University, a professorial lecturer of international affairs at the Elliott School of International Affairs – George Washington University, and principal of the Center for Macroeconomics and Development. He is a former vice-president and a former executive director at the World Bank, a former executive director at the International Monetary Fund and a former vice-president at the Inter-American Development Bank. He is also a former deputy minister for international affairs at Brazil’s Ministry of Finance and a former professor of economics at University of São Paulo and University of Campinas, Brazil.

The Islamic Development Bank (IsDB) Group hosted a webinar on the impact of the COVID-19 pandemic on the global investment outlook, which was organized in collaboration between the United Nations Conference on Trade and Development (UNCTAD) and the Country Strategy and Cooperation (CSC) Department, IsDB on 17th November 2020 to discuss the impact of COVID-19 on FDI and trade in OIC member countries.

The main objective of the webinar is to present the key findings of the World Investment Report 2020 – International Production Beyond the Pandemic with a highlight on FDI trends in foreign direct investment (FDI) worldwide, at the regional and country levels and emerging measures to improve its contribution to development. In addition to presenting IsDB Group Strategy during COVID-19 and its impact on OIC Member Countries and Investment Promotion Agencies (IPAs).

The Webinar also proposed adopting policies and strategies to revive investment and trade in member states to advance investment promotion activities, in order to support the IsDB Group efforts to assist Investment Promotion Agencies (IPAs) in member countries by assisting them in devising appropriate investment and trade policy responses to the ongoing pandemic

Mr. Oussama Kaissi, CEO of the Islamic Corporation for the Insurance of Investment and Export Credit (ICIEC), stated that “the COVID-19 pandemic has created a devastating global health crisis. According to UNCTAD’s 2020 World Investment Report, global flows of foreign direct investment (FDI) will be under acute pressure this year as a direct result of the pandemic. In order to combat these implications in member countries, IsDB and its group members have implemented a number of initiatives to maintain trade and investment flows. ICIEC will be an important part of the long-term recovery, supporting the growing demand for risk mitigation solutions”.

Mr. James Zhan, Director, Investment & Enterprise Division, UNCTAD, made a presentation which highlighted the key findings and policy recommendations found in its World Investment Report 2020: International Production Beyond the Pandemic.

Mr. Amadou Diallo, the Acting Director-General, Global Practices at the Islamic Development Bank in his speech stated that during COVID-19, the Bank provided technical assistance programs for the Islamic Development Bank Group such as RCI and ITAP to support the Member Countries by assisting them in developing suitable plans for investment and trade policy to confront the ongoing Corona pandemic. This is in the framework of a tripartite approach centered around the “response, recovery and rebuilding” pillars.

Mr. Mohammed Bukhari, Senior Investment Promotion & Regional Cooperation Specialist, CSC Dept., IsDB delivered a presentation on the impact of COVID-19 on MCs, particularly in foreign direct investment (FDI), domestic investment and investment promotion agencies (IPAs).

It is noteworthy that the private sector institutions of the Islamic Development Bank Group played an important role during COVID-19, as Mr. Asheque Moyeed, Division Head, Infrastructure & Corporate Finance, the Islamic Corporation for the Development of the Private Sector (ICD) made a presentation which focused on the efforts related to promoting investment in member countries, where the IsDB Group private sector institutions pledged with IsDB to provide $ 700 million to stimulate investment, finance trade, investment insurance and export credit in member countries. Two D-8 Egypt and Turkey are going to utilize around $270 million of this package.

The webinar brought together over 500+ participants from 113 countries, including government officials, Presidents & CEOs of local/international private sector companies, multilateral and financial institutions, individual investors, entrepreneurs, chambers of commerce & Industry, business associations, and investment promotion agencies

Even before the coronavirus pandemic, the oil and gas industry was faced with slumping prices. However, with a record collapse in oil demand amid the coronavirus lockdown, the COVID-19 crisis has further shaken the market, causing massive revenue and market cap drops for even the largest oil and gas companies.

According to data presented by StockApps.com, the top five oil and gas companies in the United States lost over $307bn in market capitalization year-over-year, a 45% plunge amid the COVID-19 crisis.

Market Cap Still Below March Levels

Global macroeconomic concerns such as the US-China trade war and the oil overproduction set significant price drops even before the coronavirus outbreak. A standoff between Russia and Saudi Arabia in the first months of 2020 sent prices even lower.

After global oil demand plunged in March, Saudi Arabia proposed a cut in oil production, but Russia refused to cooperate. Saudi Arabia responded by increasing production and cutting prices. Shortly Russia followed by doing the same, causing an over 60% drop in crude oil prices at the beginning of 2020. Although OPEC and Russia agreed to cut oil production levels to stabilize prices a few weeks later, the COVID-19 crisis already hit. Statistics show that oil prices dropped over 40% since the beginning of 2020 and are hovering around $40 a barrel.

Such a sharp fall in oil price triggered a growing wave of oil and gas bankruptcies in the United States and caused a substantial financial hit to the largest gas producers.

In September 2019, the combined market capitalization of the five largest oil and gas producers in the United States amounted to $674.2bn, revealed the Yahoo Finance data. After the Black Monday crash in March, this figure plunged by 45% to $373bn. The following months brought a slight recovery, with the combined market capitalization of the top five US gas producers rising to over $461bn in June.

However, the fourth quarter of the year witnessed a negative trend, with the combined value of their shares falling to $367bn at the beginning of this week, $6.2bn below March levels.

Exon Mobil`s Market Cap Halved in 2020, Almost $155bn Lost YoY

In August, Exxon Mobil Corporation, once the largest publicly traded company globally, was dropped from the Dow Jones industrial average after 92 years. As the largest oil and gas producer in the United States, the company has suffered the most significant market cap drop in 2020.

Statistics indicate the combined value of Exxon Mobil`s shares plunged by 52% year-over-year, falling from almost $300bn in September 2019 to $144bn at the beginning of this week.

Phillips 66, the fourth largest gas producer in the United States by market capitalization, witnessed the second-largest drop in 2020. Statistics show the company`s market cap dipped by 49.6% year-over-year, landing at $22.9bn this week.

The Yahoo Finance data revealed that EOG Resources lost over $21bn in market cap since September 2019, the third-largest drop among the top five US gas producers.

Conoco Phillips witnessed a 42% drop in market capitalization amid the COVID-19 crisis, with the combined value of shares plunging by almost $30bn year-over-year.

Statistics show Chevron witnessed the smallest market cap drop among the top five companies. At the beginning of this week, the combined value of shares of the second-largest US gas producer stood at $141.5bn, a 36.9% plunge year-over-year.

The webinar entitled, “IsDB Group Private Sector Action Response to COVID-19” will discuss the challenges facing the private sector and global economy during the COVID-19 outbreak.

30 June, 2020, Dubai, UAE – The Islamic Development Bank Group in partnership with the UAE Ministry of Economy and Annual Investment Meeting, will conduct a live webinar entitled “IsDB Group Private Sector Action Response to COVID-19” on the 6th of July at 01:00 PM (KSA Time) to discuss the challenges facing the private sector and global economy during the COVID-19 outbreak.

H.E. Eng. Sultan Al Mansoori

The live session will also present the immediate joint action response of the IsDB Group Private Sector Entities namely, the Islamic Corporation for Insurance of Investments and Export Credits (ICIEC), Islamic Corporation for the Development of the Private Sector (ICD), and the International Islamic Trade Finance Corporation (ITFC), in order to overcome the COVID-19 pandemic.

The webinar will discuss the future outlook to overcome the COVID-19 pandemic. In addition, the webinar will highlight the IsDB Group’s US$2.3 billion Strategic Preparedness and Response Programme for COVID-19 under its 3Rs approach “Respond, Restore and Restart”.

The keynote speakers who will share their in-depth perspectives in the webinar are Mr. Ousama Kaissi, the Chief Executive Officer of the Islamic Corporation for the Insurance of Investment and Export Credit (ICIEC); Mr. Ayman Sejiny, the CEO & General Manager of the Islamic Corporation for the Development of the Private Sector (ICD), Eng. Hani Salem Sonbol, the Chief Executive Officer of the International Islamic Trade Finance Corporation (ITFC) and Ms. Cornelia Meyer, the Chairman & CEO of Meyer Resources.

Mr. Ousama Kaissi, the Chief Executive Officer of The Islamic Corporation for the Insurance of Investment and Export Credit (ICIEC) and one of the keynote speakers in the webinar, stated: “While the disruption to global trade and investment flows is unavoidable due to the unprecedented nature of the coronavirus pandemic, it is essential that institutions with the mandate and means to stabilize the trade ecosystem during the crisis heighten their efforts to do so. ICIEC is honoured to be a part of this webinar with the UAE Ministry of Economy and our IsDB Group peers in order to share how we are employing our multilateral insurance solutions toward the collective recovery of member countries.”

H.E. Dr. Bandar Hajjar

“The private sector can play a pivotal and proactive role to close funding gaps in the COVID-19 response. It is capable to minimize short-term risks to employees and long-term costs to businesses and the economy as a whole. ICD will work closely with 100+ local and regional financial institutions in its network to provide necessary support so they can continue to fund private sector, particularly SMEs in affected sectors within the markets they operate in” stated Mr. Ayman Sejiny, the CEO of the Islamic Corporation for the Development of the Private Sector (ICD), and one of the keynote speakers in the webinar.

Eng. Hani Salem Sonbol, the Chief Executive Officer of the International Islamic Trade Finance Corporation (ITFC) and one of the keynote speakers in the webinar, stated: “Since the outbreak of the pandemic, ITFC has moved quickly to put in place emergency financing measures to ensure that member countries continue to receive the support needed. Our COVID-19 ‘Rapid Response Initiative’ (RRI) has made US$ 300 million immediately available. This has facilitated the immediate access to medical equipment, the supply of staple foods and critical energy needs. Continuing to work closely with IsDB and partners, ITFC is moving forward with its Recovery Response Plan (RRP) with the provision of US$550 million for deployment over the next two years. The RRP is aimed at fixing the socio-economic damage which is expected to last longer than immediate impact of the virus; including the provision of lines of financing to fund the private sector and SMEs.”

“It is a great privilege to be in collaboration with the UAE Ministry of Economy and Islamic Development Bank Group in organizing this live webinar session that will tackle the major challenges currently being confronted by the private sector and the global economy as a whole,” Mr. Walid A. Farghal, Director General of the Annual Investment Meeting mentioned.

“The private sector is indispensable to economic growth. In fact, it contributes up to 90 per cent of employment and provides over 80 per cent of government revenues in developing countries. Thus, it is essential to highlight this huge initiative by the IsDB Group that enables the sectors adversely affected by COVID-19 to continue their business activities,” he furthered.

During the webinar, 3 online initiatives will be launched jointly by IsDB Group Private Sector Entities and AIM. These initiatives will support the private sector, trade and exports in OIC member countries and will be focusing on:

Digital Country Presentations: to promote and showcase the investment and trade opportunities in OIC member countries which will serve as a virtual gathering and strategic innovative platform to support the investors, government agencies, private institutions, investment promotion agencies to discuss the best possible means to attract FDI.

Startups Virtual Pitch Competition: to connect Startups globally and support them in meeting potential partners and investors from other parts of the world.

MADE IN…..SERIES: this digital platform is open to all SMEs who want to showcase and present their local products, project and services to international audience.

The webinar will gather more than 700 participants from multiple sectors across the globe such as government officials, Chairmen, Presidents & CEOs of local and international companies, multilateral and financial institutions, Chambers of Commerce & Industry, business associations, investment promotion agencies, individual investors, and entrepreneurs.

About the Islamic Corporation for the Insurance of Investment and Export Credit (ICIEC)

Established 26 years ago in 1994 as a multilateral institution and member of the Islamic Development Bank Group, ICIEC was tasked to promote cross-border trade and foreign direct investments (FDI) in its Member Countries. To fulfill its mandate, ICIEC provides risk mitigation solutions to Member Country exporters. By protecting them from commercial and political risks, exporters are enabled to sell their products and services across the world. The multilateral credit insurer also provides risk protection to investors from across the world that seeks to invest in ICIEC’s Member Countries. To promote the sustainable economic development of its Member Countries, ICIEC – on a limited basis – can also support international exporters selling capital goods or strategic commodities to ICIEC’s Member Countries. In addition to its core business, ICIEC also offers technical assistance to Member Countries’ Export Credit Agencies. ICIEC’s mission is to make trade and investment between Member Countries and the world more secure through the Shariah-compliant risk mitigation tool. Its vision is to be recognized as the preferred enabler of trade and investment for sustainable economic development in Member Countries. ICIEC is the only multilateral export credit and investment insurance corporation in the world that provides Shariah-compliant insurance and reinsurance solutions. Today, ICIEC supports trade and investment flows in 47 Member Countries spanning across Europe, Asia, Middle East and Africa. Its target clients are corporates (both exporters and investors), banks and financial institutions as well as Export Credit Agencies and insurers.

About the Islamic Corporation for the Development of the Private Sector (ICD)

ICD is a multilateral development organization and a member of the Islamic Development Bank (IsDB) Group. The mandate of ICD is to support economic development and promote the development of the private sector in its 55-member countries through providing financing facilities and/or investments in viable projects sponsored by eligible enterprises in accordance with the principles of Shari’ah. ICD also provides technical assistance and advisory services to member countries and their public and private enterprises with a view to improving the environment for private investment, facilitating the identification and promotion of investment opportunities, privatization of public enterprises and the development of the Islamic capital markets. ICD applies Fintech to make finance more efficient and inclusive. ICD set up a platform built and centered on ICD relationship with 119 Financial Institutions. Through them, the IsDB Group in general and ICD in particular leverage access to the country and avail financing opportunities. For more information about ICD, visit www.icd-ps.org.

The International Islamic Trade Finance Corporation (ITFC) is a member of the Islamic Development Bank (IsDB) Group. It was established with the primary objective of advancing trade among OIC Member Countries, which would ultimately contribute to the overarching goal of improving socioeconomic conditions of the people across the world. Commencing operations in January 2008, ITFC has provided more than US$51 billion to OIC Member Countries, making it the leading provider of trade solutions for the Member Countries’ needs. With a mission to become a catalyst for trade development for OIC Member Countries and beyond, the Corporation helps entities in Member Countries gain better access to trade finance and provides them with the necessary trade-related capacity building tools, which would enable them to successfully compete in the global market.

About the Islamic Development Bank Group Business Forum (THIQAH)

The Islamic Development Bank Group Business Forum (THIQAH) is the window of IsDB Group that facilitate contact and coordination between entities concerned of the IsDB Group and private sector firms and related institutions in IsDB Group member countries. The main objective of THIQAH is to establish a unique and innovative platform for dialogue, cooperation and inclusive partnership for business leaders committed to partnering in promising investment opportunities. THIQAH’s vision is to position itself as the leading business platform of the IsDB Group serving the private sector and maximizing the achievements of successful investment projects. Through facilitation and catalyst roles, THIQAH will be leveraging IsDB Group’s resources to offer necessary services and confidence to investors and to establish strategic partnerships with the leaders of the private sector in order to capitalize on their expertise and know-how on one hand, and to synergize with IsDB Group entities on the other. The primary focus will be on maximizing cross-border investment among member countries to be supported by IsDB Group’s financial products and services. (www.idbgbf.org).

About Annual Investment Meeting (AIM)

Annual Investment Meeting (AIM), the World’s Leading Investment Platform in the Middle East and North Africa, will hold its 10th at the Dubai World Trade Centre, Dubai, United Arab Emirates.

Under the theme ‘Investing for the Future: Shaping the Global Investment Strategies’, AIM will gather high-ranking government officials, decision makers, corporate leaders, policy makers, businessmen, regional and international investors, entrepreneurs, leading academics and investment experts to address the global challenges of securing viable investment aimed at contributing to economic growth.

AIM has evolved from assisting emerging economies to attract FDIs. On its 10th edition, AIM will embrace a bigger challenge of enabling economic growth through its five pillars – FDIs, Startups, Future Cities, SMEs, Foreign Portfolio Investment, and special event One Belt and One Road.

AIM 2019 saw the participation of over 16,000 visitors, 436 exhibitors and co-exhibitors, 66 high-level dignitaries, more than 150 experts and investment specialists, and 143 country representations.

Union Bank of the Philippines (UnionBank) has been ranked as the second most helpful bank in Asia-Pacific during the coronavirus crisis – the only Philippine bank in the top 20 list.

UnionBank was next only to KakaoBank, South Korea’s largest digital-only bank, according to the BankQuality Consumer Survey on Retail Banks – an online survey conducted last April 1-30, 2020 and covering total 11,000 respondents, with 1,000 each coming from China, Hong Kong, India, Indonesia, Malaysia, Philippines, Singapore, South Korea, Taiwan, Thailand and Vietnam.

The respondents, aged between 18 to 65 and who have at least one bank account each, chose the banks most beneficial to them amid the ongoing pandemic because of their contactless nature and digital services.

UnionBank was ranked higher than international banks such as HSBC, Citibank, DBS, CIMB, United Overseas Bank and OCBC, among others.

UnionBank president and CEO Edwin Bautista expressed gratitude for the public’s recognition of the bank’s quick, sincere and relentless efforts to help alleviate their plight in this difficult time.

“It warms our hearts to know that our customers recognize and value our heroic efforts during this crisis. The coronavirus pandemic has brought the world an unprecedented disruption, but with each of us doing our share, we will weather this challenge – no matter how massive it can be,” Bautista said.

Since the start of the quarantine period, UnionBank boosted its mobile and web banking platforms for retail and corporate customers namely UnionBank Online and The Portal, respectively, to enable clients to safely do their banking transactions from home.

UnionBank was also among the first banks to waive its online fund transfer fees, and deployed its Bank On Wheels to bring its bank branches at the doorstep of its customers.

“I would like to also thank our very hardworking and selfless UnionBankers – frontliners all – who have been doing their utmost during this pandemic to deliver safe, consistent and full service digital banking to our customers, for this accolade,” Bautista added.

The bank’s fintech arm UBX, has facilitated the release of cash subsidies through the deployment of mobile automated teller machines (ATMs) to its rural bank partners and financial cooperatives where beneficiaries of the government’s Social Amelioration Program can withdraw their money quickly.

UBX has also begun linking its rural bank members to its new network that includes Cebuana Lhuillier, LBC, Palawan Express and PeraHub. This enables customers of these rural banks to send funds and payments to over 11,000 branches of the four remittance centers nationwide.

What happens to confidential waste while working from home?

With employees working from home because of the Covid-19 outbreak, how safe is the information they’re accessing and disposing of now it’s out of the office?

According to one specialist waste handling organisation, remote working means new headaches for companies and their data security.

UK waste collection agency BusinessWaste.co.uk knows that even during the crisis of a pandemic, confidential waste must be disposed of correctly in order to protect businesses and their customers from fraud or blackmail.

“Even if people are working from home, they need to be mindful that any waste they create needs to be destroyed in the same ways it would if they were in the office,” says BusinessWaste.co.uk company spokesperson Mark Hall. Companies could still be in line for massive fines if they get it wrong, Hall warns.

What counts as confidential waste?

Essentially, confidential waste refers to documents possessed by any company that can expose discrete information about suppliers, customers, or employees.

“Basically, if it details any information about the nature of your work or anyone associated, then it counts as confidential information which will need proper disposal,” says spokesman Mark Hall.

However, it can be very tricky to distinguish what counts as confidential waste, as many businesses work with different mediums of materials.

BusinessWaste.co.uk has compiled a list of different types of confidential waste, making it easier to understand which work-related items will need expert disposal.

Personnel files and contracts – including CVs and application letters

Financial records – such as order forms, invoices, bills and statements

Health and social care records

Criminal Records

Business cards, ID badges, and security passes

Letters, memos, and other items containing names and addresses.

New business proposals and business plans

Used notebooks

Product samples or profiles

Research data

Diaries

Photographs

“If you’re working from home, you need to be aware that any of these resources could contain confidential details which could be dangerous in the wrong hands,” says Hall.

“So please make sure you or your staff don’t throw this information into the household waste!”

What could happen if it’s not disposed of properly?

Failing to dispose of confidential waste can lead to a variety of outcomes, ranging from prosecutions under the law to identity theft and fraud.

“Your company could fall victim to industrial espionage, so it’s really important to make sure that private information cannot be leaked to rival companies through improper disposal,” says Hall.

Although it might be easier to just chuck all rubbish into your household waste bin, there are legal implications such as breaching the UK 1988 Data Protection Act, which regulates the collecting, storing, and destroying of confidential data.

Any companies that fail to oblige the act can face crippling fines from the UK data watchdog, the Information Commissioner’s Office.

“This is serious stuff that could ruin a company’s reputation and lose customers,” says Hall, “and if you’re the one discovered to be doing it, you could be fired.”

Confidential waste needs to be disposed of by a licensed waste removal company in order to comply with the latest laws and guidelines.

Actions you can take now

BusinessWaste.co.uk recommends that all members of staff be reminded about company policies regarding waste, and firmly told not to chuck any work materials into their household rubbish.

Mark Hall says that in an ideal world, sensitive information should not leave the office, so the best thing for businesses to do is to try to restrict what is essential and needs to be taken home.

Another suggestion from Hall is to make as many work tasks computer-based as possible, with sensitive files only accessible from a secure device approved by your company.

“The best thing you can do if you’re unsure is to keep all information secure and together at your home workspace, and when it is safe to do so, take it all back to work for proper disposal,” says Hall.

As political leaders across Europe are contemplating how to best prepare the restart of our economies, European Fintechs Loyaltek and Paynovate launch the Unity Card (unitycard.eu): an initiative enabling authorities to financially support certain segments of the population, such as the most underprivileged, but also to specifically target local retailers and merchants who’ve had to close their businesses.

The special payment card, which will exceptionally be free to municipalities as the first, local level of power, can be delivered anywhere on the Old Continent in as fast as 2-4 weeks and avoids cumbersome logistics and administration, allowing for effective, ultra-targeted, monitorable and evolutive socio-economic measures on the road to economic recovery.

Brussel, 24 april 2020. As the Corona curves are slowly but surely starting to flatten, the focus is gradually shifting towards the next challenge: relaunching the economy. Whilst national governments and international institutions across Europe and the world are announcing unprecedented crisis measures, it remains to be seen if these will be enough, and especially, whether the aid can be deployed quickly enough to save those in need today. Therefore, decisive action needs to be taken today rather than tomorrow.

With a view to this, European FinTech pioneers and veterans Loyaltek and Paynovate are teaming up in a unique proposal to political leaders, with the aim of offering citizens much needed and rapid financial support by means of the Unity Card. As innovative as it is useful, this debit card can be limited for use in a certain geographical area (e.g. one municipality) as well as a certain types of predetermined shops or businesses, in this case those that have been forced to close during the current crisis: hotels, restaurants, bars, hairdressers, DIY-stores, clothes stores… As such, it is the perfect instrument to stimulate the local economy and prevent the money disappearing to foreign e-commerce websites, being sent to family abroad, or saved.

“Whether it’s to support merchants who have had to close their business or to help a mother feed her children: our leaders, from municipal to national level, are looking for ways to mitigate the effects of the lockdown and prepare for a return to normal life and economic recovery,” explains Robert Masse, founder and CEO of Loyaltek and expert in the field of card payments. “But time is running out, and the question arises as to how to allocate these various resources as quickly and efficiently as possible, while at the same time avoiding any risks of fraud and ensuring that public money serves its intended purpose, to the extent of creating a win-win situation and benefiting society as a whole.”

The Unity Card has a maximum value of €250 and works just like a regular debit card on payment terminals. The validity period can be adapted in function of the needs and intended support. Users can check the remaining value thanks to a QR code on the back, while an extranet allows the issuing authority to monitor, analyse, manage and even adjust the way its cards are being used, all in real-time. And thus, once again in this crisis, it’s new technologies that are offering relief in a situation which at first seemed insoluble.

“In a spirit of social commitment, our R&D teams wanted to make themselves useful against the horrors of the Corona virus. Ultimately, it’s the pragmatism and the potential of this solution which convinced us to set up the necessary partnerships to deploy it throughout Europe,” concludes Robert Masse. “The name, which of course stands for solidarity, came naturally, and we have decided to offer the first 5,000 cards to each of the municipalities that want to work with it, given that they’re the ones closest to the situation on the ground. Implementation costs are kept to a minimum and amount to a fraction of the usual costs of similar ‘traditional’ measures. Moreover, we do not take any margin on the transactions.”

The solution proposed by Loyaltek and Paynovate has proven its worth before in Germany at the time of the migration crisis, when authorities distributed thousands of similar cards to manage the allowances of Syrian refugees, allowing them to provide in their most basic needs by purchasing from local merchants.

The appearance of the Unity Card can be personalised if necessary. It is distributed either directly to the beneficiaries or by group transmission to the competent authority, which can then further distribute it. The payments made by citizens with the card are managed together with the rest of the merchants’ payment traffic, while cardholder support is ensured by Loyaltek or the ‘customer’ himself, i.e. the issuing authority.

Loyaltek NV is a European leader in limited range cards and manages numerous gift card and professional expense cards programmes in 14 countries. Its clients include Sodexo, Ingenico, Total and a great number of major commercial real estate players. They call on Loyaltek’s expertise for specific and technically advanced projects.

Paynovate NV is one of the six Belgian issuers of electronic money, regulated by the National Bank of Belgium and authorised to issue payment instruments in all European countries. Paynovate is also a principal member of Visa and Bancontact.

In response to the Philippine government’s “Stay At Home” directive as part of the ongoing enhanced community quarantine, Union Bank of the Philippines (UnionBank) continues to process a growing number of digital transactions and remains business-as-usual (BAU), throughout the ECQ.

For the month of March, UnionBank logged a nearly 160% in

daily sign-ups to its online and mobile banking portals, and enabled more than

500,000 credit card transactions and well over 1 million Instapay and PesoNet

fund transfer transactions. Importantly, the bank waived all its fees on

InstaPay and PesoNet since the start of the ECQ and has extended this to April

30.

Most significantly, UnionBank also registered a tremendous

surge in new accounts opened “100% digitally” through the UnionBank Online

platform, as this was 2700X higher than year-ago levels.

These

robust figures come amid reports from several consumer monitoring groups that

the behavior of banking customers may be changing, preferring to use digital

channels during the lockdown.

UnionBank

president and CEO Edwin Bautista said the coronavirus crisis could be the

turning point in customers’ shift-to-digital –

to safely access their funds, do transfer, make payments and apply for credit.

“This

represents a tremendous new opportunity for banking in the country as this

should reduce the number of Filipinos who remain unbanked. As this

happens, we at UnionBank are fully prepared with the digital infrastructure

already in place to offer full banking services to more people, more

conveniently and more cost-effectively,” Bautista said.

Along

with its digital platforms that enable the public to bank from home, UnionBank

also rolled out its 5G-enabled mobile van

called 5G-Bank On Wheels (5G-BOW) to serve people’s banking needs during the

ECQ.

With its 5G-BOW clients can withdraw, pay bills, transfer funds,

open an account and do balance-inquiries with faster, more robust bandwidth and

internet connections, powered by its unique 5G technology.

In terms of its brick-and-mortar branches, UnionBank was able

to keep 94% of its branches open, outside of those in medical

quarantine and local lockdown areas; while safely keeping close to 90% of

employees working from home in compliance with government guidelines.

There aren’t many sports that have been hit harder by the

outbreak of COVID-19 than horse racing. Some of the biggest events on the

racing calendar have already been lost, while some remain hanging by the

thinnest of tightropes.

Racing continues to take place in Australia, the USA and

various parts of Europe, but not all countries have been as fortunate. The

lucrative industry has been hit as most of businesses have, even though online

gambling seems to be on the rise due to the self-quarantine inflicted to

millions of people.

However, which events

on the horse racing calendar have been lost, which ones have face criticism,

and which have been re-arranged for a later date?

Kentucky Derby

Few would argue against the Kentucky Derby being the biggest

race of the year, and it is huge for the American industry. That is highlighted

by the amount of money that is gambled on the race day, with the 2019 event

eclipsing records. The 14-race card saw over $227.5 million gambled, while the

Kentucky Derby itself saw around $150 million worth of bets. The Kentucky Derby

is the most attended event on the US racing calendar, and that meant that cancelling

the event altogether wasn’t an option.

Instead, for the first time this year, the Kentucky Derby

will be taking place as the final event of the Triple Crown as opposed to the

first. The event was cancelled in March, as it was revealed that it would

instead take place on the 5th September. Nonetheless, you can still place your bets on the

Kentucky Derby through Twinspires.com.

This marks the first time since 1945 that the event has been

suspended. The Preakness Stakes and Belmont Stakes are still slated to go ahead

on their original dates.

The Grand National

The most lucrative betting day in the United Kingdom didn’t

go ahead as planned for the first time since the Second World War. The decision

to cancel

the event meant that the betting industry in the UK lost half a billion

pounds, while Tiger Roll missed his opportunity at making history by becoming

the first horse to win three successive Grand Nationals.

The horse racing industry did still put a show on for racing

fans however on Grand National day on the 4th April, as a virtual race was

broadcast, with all proceeds going towards the NHS. The event raised £2.6

million for the service, while the virtual race was won by Potters Corner.

Cheltenham Festival

Just a few weeks before the Aintree Festival, there was the

Cheltenham Festival, which is the most prestigious jumps festival of the year.

That event went ahead as planned, but organisers have already drawn criticism

for their decision to do so. There were

reported symptoms shown by some that attended; including

Andrew Parker Bowles.

However, the Jockey Club reiterated that they accurately

followed all the guidelines that were put in place by the British government at

the time. The Cheltenham Gold Cup on Friday 13th March was the final noteworthy

sporting event to take place in the UK as the Premier League announced that it

would be suspending fixtures on the same day.

Royal Ascot

The biggest flat festival of the season in the UK is still

planning to go ahead as planned, but this year it will take place behind closed

doors. The event is famous for those attending to get dressed up smart, while

Queen Elizabeth has been known to visit most days. The festival is due to begin

on the 16th June, but the announcement that it would be taking place behind

closed doors was made on the 7th April.

The organisers admitted that they were pressing ahead with

the event, but no spectators would be able to attend. However, the statement

released also admits that there is still a chance that the event may not take

place at all. The organisers will have to follow the guidelines by the British

government and the BHA, who have currently suspended all racing in Britain

until the end of April.

We are living in unprecedented times with a

global pandemic that has killed hundreds of thousands and countries all over

the world ordering their citizens to self-quarantine.

With the suspension of all but the most critical

industries business owners and governments alike are preparing for the arrival

of a global recession – one which is feared to be far more devastating than

the Great Depression and the 2009 Global Financial Crisis.

Given that COVID-19 spreads via water droplets

expelled from an infected person,social distancing measures have been

implemented in order to help break the chain of infection with many governments

enforcing a strict curfew.

Now with the United States becoming the

epicenter of the pandemic, entire industries including casinos have been left

in a lurch. According to a report by the American Gaming

Association (AGA), the industry is slated

to lose an estimated $21.3 billion in direct spending from consumers

alone.

Here, we take a look at how we can expect the

outbreak of COVID-19 to change the face of online gambling.

1. A Massive Increase in Customers

In early-April, Nevada’s

Clark county reported more than 1000

COVID-19 cases and almost 30 deaths which prompted Governor Sisolak to order a shutdown of

all casinos in the state despite severe pushback from various stakeholders

including the Mayor of Las Vegas, Carolyn Goodman (I).

With almost all casinos in the United States

shutdown, punters all over the country have turned to online gambling for all

of their gaming needs. This has resulted in a windfall for online casinos

everywhere with a nearly 50% increase in

revenue with punters avoiding land-based casinos in favour of online ones.

Given that the COVID-19 pandemic has shown no

signs of letting up and with a vaccine far off, the remainder of 2020 and 2021

is set to be a good year for the online gambling industry.

As the global economy grinds to a halt and

uncertainty reigns supreme, many have begun to ask the question – will things

ever be the same again? According to many experts, the answer is a resounding

no.

The highly contagious nature of the COVID-19

virus and the variety of health complications means that social distancing

measures will have to be practiced for the foreseeable future or until a

vaccine is developed – which is highly unlikely.

Until a solution is found, it is highly likely

that online casino betting will be able to enjoy an unprecedented increase in customers.

2. The Entry of New Competitors

While some may point out that casinos in Macau –

the world’s largest gambling hub were able to resume operations after just 15

days, the stark reality is that things are far from normal. Casino floors are

relatively empty and foot traffic remains low with many punters staying away

from crowded areas.

Given the relatively low-barriers for entry and

a market filled with investors hungry for opportunity, it is only a matter of time before new competitors begin

appearing on scene. This can potentially be a problem for current online

casinos who may want to consider diversifying their range of games offered.

With sports betting also affected by the lockdown,

punters have begun turning towards online casinos and slot games for their

gambling needs which may in turn encourage bookmakers to open up their own

online casinos in order to capitalize on shifting market demands.

3. Stricter Compliance

Casinos and other gambling outlets have always

been closely monitored and regulated by government bodies given the nature of

the business. Now with the economy taking a turn for the worst and with jobs at

stake, people are likely to be more anxious and stressed which in turn leads to

compulsive gambling and other risky behavior.

This has forced governments everywhere to

introduce more stringent regulations with regards to gambling, these measures have included

restricting advertising, minimizing payouts and even banning gambling outright

in some areas.

Given the current state of affairs and the

increased levels of vigilance, online casinos and gaming sites may begin

imposing limits on bet sizes and practice more thorough screening of

punters.

4. Potential cash flow issues

Whilst the online casino business is and has

always been a solid one, it is not entirely recession-proof. As businesses all

over the world shut down or scale back on their operations, employees and

business owners everywhere face the very real prospect of losing a significant

portion of their incomes.

This in turn overlaps onto the online betting

industry as punters begin to suffer from problems related to cash flow.

Initially, the effects may not be tangible as we are yet to feel the true

impact of a pending global recession.

Only when businesses begin to shut down and

unemployment numbers rise 6 to 8 months down the line, will we begin to see a

drop in revenue and takings. Consequently, operators should seriously consider

putting aside cash reserves for the lean months ahead in order to stay afloat.

As the old proverb goes, “All Good Things Must

Come to an End”, so will the windfall from the sudden influx of new punters.

The COVID-19 pandemic is unlike anything that humanity has seen in over a

century and even the most resistant of industries will not be safe.