We are living in unprecedented times with a global pandemic that has killed hundreds of thousands and countries all over the world ordering their citizens to self-quarantine.

With the suspension of all but the most critical industries business owners and governments alike are preparing for the arrival of a global recession – one which is feared to be far more devastating than the Great Depression and the 2009 Global Financial Crisis.

Given that COVID-19 spreads via water droplets expelled from an infected person,social distancing measures have been implemented in order to help break the chain of infection with many governments enforcing a strict curfew.

Now with the United States becoming the epicenter of the pandemic, entire industries including casinos have been left in a lurch. According to a report by the American Gaming Association (AGA), the industry is slated to lose an estimated $21.3 billion in direct spending from consumers alone.

Here, we take a look at how we can expect the outbreak of COVID-19 to change the face of online gambling.

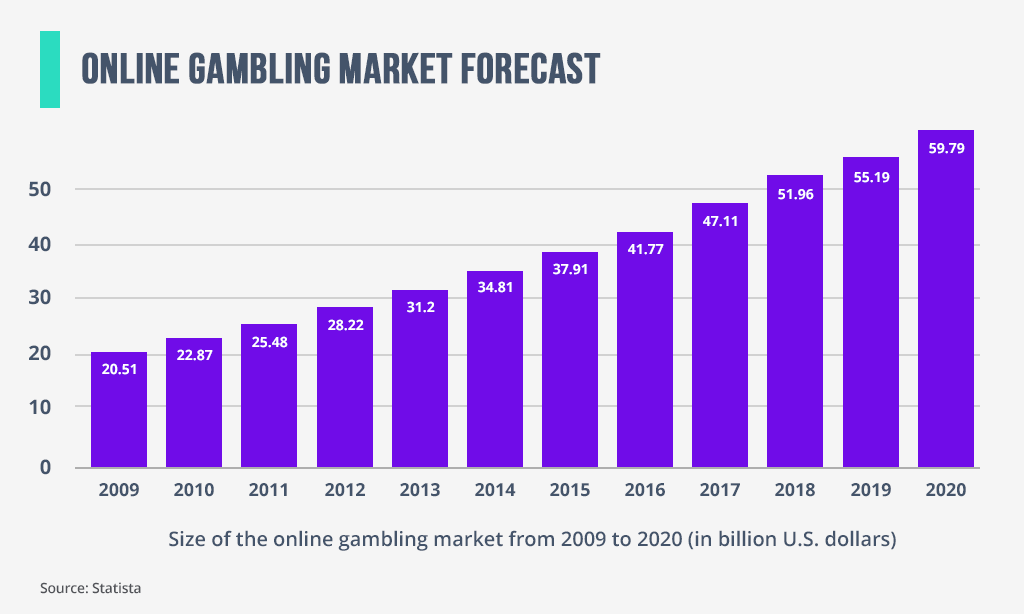

1. A Massive Increase in Customers

In early-April, Nevada’s Clark county reported more than 1000 COVID-19 cases and almost 30 deaths which prompted Governor Sisolak to order a shutdown of all casinos in the state despite severe pushback from various stakeholders including the Mayor of Las Vegas, Carolyn Goodman (I).

With almost all casinos in the United States shutdown, punters all over the country have turned to online gambling for all of their gaming needs. This has resulted in a windfall for online casinos everywhere with a nearly 50% increase in revenue with punters avoiding land-based casinos in favour of online ones.

Given that the COVID-19 pandemic has shown no signs of letting up and with a vaccine far off, the remainder of 2020 and 2021 is set to be a good year for the online gambling industry.

As the global economy grinds to a halt and uncertainty reigns supreme, many have begun to ask the question – will things ever be the same again? According to many experts, the answer is a resounding no.

The highly contagious nature of the COVID-19 virus and the variety of health complications means that social distancing measures will have to be practiced for the foreseeable future or until a vaccine is developed – which is highly unlikely.

Until a solution is found, it is highly likely that online casino betting will be able to enjoy an unprecedented increase in customers.

2. The Entry of New Competitors

While some may point out that casinos in Macau – the world’s largest gambling hub were able to resume operations after just 15 days, the stark reality is that things are far from normal. Casino floors are relatively empty and foot traffic remains low with many punters staying away from crowded areas.

Given the relatively low-barriers for entry and a market filled with investors hungry for opportunity, it is only a matter of time before new competitors begin appearing on scene. This can potentially be a problem for current online casinos who may want to consider diversifying their range of games offered.

With sports betting also affected by the lockdown, punters have begun turning towards online casinos and slot games for their gambling needs which may in turn encourage bookmakers to open up their own online casinos in order to capitalize on shifting market demands.

3. Stricter Compliance

Casinos and other gambling outlets have always been closely monitored and regulated by government bodies given the nature of the business. Now with the economy taking a turn for the worst and with jobs at stake, people are likely to be more anxious and stressed which in turn leads to compulsive gambling and other risky behavior.

This has forced governments everywhere to introduce more stringent regulations with regards to gambling, these measures have included restricting advertising, minimizing payouts and even banning gambling outright in some areas.

Given the current state of affairs and the increased levels of vigilance, online casinos and gaming sites may begin imposing limits on bet sizes and practice more thorough screening of punters.

4. Potential cash flow issues

Whilst the online casino business is and has always been a solid one, it is not entirely recession-proof. As businesses all over the world shut down or scale back on their operations, employees and business owners everywhere face the very real prospect of losing a significant portion of their incomes.

This in turn overlaps onto the online betting industry as punters begin to suffer from problems related to cash flow. Initially, the effects may not be tangible as we are yet to feel the true impact of a pending global recession.

Only when businesses begin to shut down and unemployment numbers rise 6 to 8 months down the line, will we begin to see a drop in revenue and takings. Consequently, operators should seriously consider putting aside cash reserves for the lean months ahead in order to stay afloat.

As the old proverb goes, “All Good Things Must

Come to an End”, so will the windfall from the sudden influx of new punters.

The COVID-19 pandemic is unlike anything that humanity has seen in over a

century and even the most resistant of industries will not be safe.